The Eye-Opening Truth: Over half of Americans don’t even know how to calculate their net worth, and nearly one-third have a net worth at or below $0. This isn’t just a statistic – it’s a wake-up call. creditkarma.com

What Is Net Worth?

It’s the sum of everything you own minus everything you owe. In other words: Assets – Liabilities = Net Worth. This single number is like your financial experience points – it shows how far you have come, and with each new level, you unlock cool new perks.

Formula:

Net Worth = Assets - Liabilities

Example:

$500 = $2000 - $1500

Why This Article?

Whether you’re a beginner just starting out or an expert fine-tuning your finances, understanding and tracking net worth is key. In this guide, we’ll explore why tracking your net worth matters – from basics like categorizing assets and debts to advanced insights on growth benchmarks, psychology, and compounding. You’ll also discover the best tools (from simple spreadsheets to cutting-edge apps) to make net worth tracking easy and even fun.

Have you ever wondered how much money you have in total? Not just the cash in your wallet or your piggy bank, but everything you own and owe? That total amount is called your net worth. Tracking your net worth is like having a financial report card, and it’s super important for a few reasons. Let’s dive in and see why keeping an eye on your net worth matters!

First, We Need to Understand What is Money?

Money is simply a tool—a magnifier that amplifies who you already are and what you already do. If you’re generous, having more money makes generosity easier; if you’re disciplined, it becomes rocket fuel, accelerating your progress toward your goals. Money itself isn’t good or bad—it’s neutral, shaped entirely by the hands that hold it. It’s like fire: it can warm your house or burn it down, depending on how you manage it. Ultimately, mastering money means mastering yourself, turning your potential into reality.

What Net Worth Isn’t

Net worth, on the other hand, is not a measure of your worth as a person, your happiness, or your success in life. It isn’t determined by how impressive your lifestyle appears, how much stuff you own, or how much you earn annually. Net worth isn’t a competition or something to flaunt; it’s not about looking wealthy but about truly being financially secure. It doesn’t automatically indicate financial wisdom—someone with high net worth can still make poor financial decisions. Above all, net worth isn’t static; it’s a snapshot of your current financial position, not your destiny. Some use it for motivation, but most importantly, it should be used as a path to self-discovery and improvement.

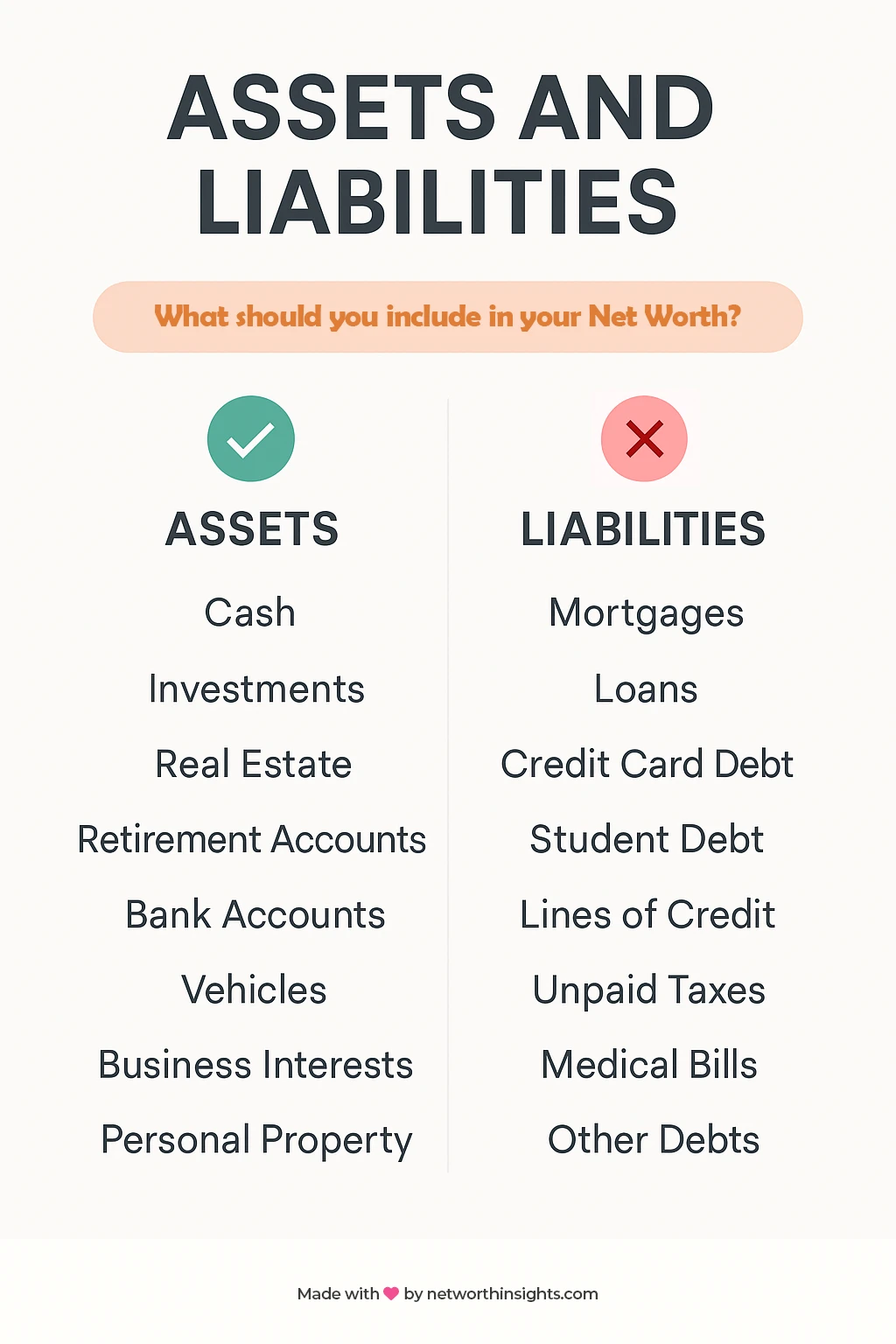

Net Worth Basics: Assets, Liabilities, and How to Calculate

- Defining Assets and Liabilities: To track net worth, you need to know what to include. Assets are everything valuable you own – cash, investments, real estate, retirement accounts, vehicles, etc.

- Liabilities are all your debts – mortgage, student loans, credit cards, car loans, etc.

- Example: Your home (asset) minus the mortgage on it (liability) contributes to your net worth. A $300,000 house with a $200,000 mortgage adds $100,000 to your net worth.

- Tip: Don’t count everyday belongings with little resale value (clothes, basic furniture) – focus on assets that truly contribute (bank balances, investments, property equity). Also exclude your monthly bills/expenses; only outstanding debts count as liabilities.

- How to Calculate Net Worth: It’s straightforward arithmetic: Total Assets – Total Liabilities. Make a list of all asset values, sum them up, then subtract all debts. The result can be positive (you own more than you owe) or negative (you owe more than you own).

- If you’ve never done this, start with a basic list: cash in the bank, investments, car value, home value, etc., and credit card balances, loans, etc. Then, do the math. Even if the number is small or negative, it’s better to know it.

- Snapshot vs. Trend: Remember, a net worth calculation is a snapshot of today. Its real power comes from tracking it over time. A single calculation is less meaningful without context. In the next section, we’ll see how monitoring changes month-to-month or year-to-year uncovers the true story of your financial progress.

(Note: This section ensures even a beginner understands net worth fundamentals. Feel free to include a simple graphic or chart illustrating assets minus liabilities equaling net worth, for visual learners.)

Goal Setting and Motivation

Turning Dreams into Targets

When you know your net worth, you can set tangible financial goals and measure progress. It’s hard to plan for “financial freedom” abstractly – but if you know your net worth today, you can set a goal for what you want it to be next year or in five years. Tracking gives specificity to your goals.

Breakdown Big Goals

Net worth tracking helps break down big goals (like buying a home, retiring early, becoming a millionaire) into incremental progress. For example, if your goal is a net worth of $100K and you’re at $40K now, seeing that progress inch up each month (50K…60K…) keeps you focused and encouraged.

Psychological Boost

There’s a behavioral psychology aspect: seeing your efforts translate into a growing net worth provides positive reinforcement. Paying off $5,000 of debt might feel abstract, but when you update your net worth and see it jump up by the same $5,000, it’s concrete proof of progress. That reward can reinforce good habits.

Relatable Analogy: This is similar to tracking weight loss or fitness milestones. Checking in regularly and seeing improvement (even small) motivates you to stick with good habits. In finance, tracking net worth can encourage you to save more, spend smarter, and invest consistently, because you can literally see the results.

Accountability

Regular check-ins with your net worth number create a sense of accountability. It’s like having a monthly financial “weigh-in.” If you know you’ll be logging your net worth, you might think twice about that impulse purchase or taking on new debt, because you’ll see the impact at month’s end. It turns abstract money moves into visible outcomes.

Achieving Milestones

Celebrating milestones becomes fun. First $0 net worth (out of debt), first $100K, etc. Many people find tracking addictive in a good way – it becomes a game where net worth is the score. In fact, personal finance communities often share net worth updates as a way to stay motivated and accountable (J. Money of BudgetsAreSexy famously shared his net worth every month for years as motivation).

Better Financial Habits and Awareness

Measure it or ignore it—there’s no middle ground.

Every time you log your net worth, you hold a mirror up to your money habits. Suddenly, that “harmless” $100 DoorDash splurge isn’t just a line on your credit card—it’s a visible dent in your wealth. Visibility breeds accountability, and accountability sparks change.

Spending vs. Investing: Flip the Script

- Phone or Fortune? A $1,000 iPhone feels cool—until you see it as a $1,000 dip in net worth.

- Compound Confidence: Drop the same grand into an index fund and watch your net worth tick upward. Tracking reframes choices from “Can I afford this?” to “Will this grow my wealth?”

Debt Reduction Becomes a Game

- Each student‑loan payment shrinks liabilities and nudges net worth higher. Seeing that instant win‑win effect turns payoff into a score‑keeping sport, not a slog.

- Want motivation? Chart your debt‑to‑net‑worth ratio monthly and chase a new personal best.

The 360‑Degree View

- Focusing on one lever (e.g., hammering a 3 % mortgage) while ignoring higher‑yield opportunities (like maxing a 401(k)) is like training only biceps and skipping legs—imbalanced and ineffective.

- Net worth tracking forces every asset and liability onto the same scoreboard, revealing the true MVP moves.

Behavior Loops That Stick

- Behavioral‑finance studies show dieters who weigh in often lose more weight; the same feedback loop works for money.

- Frequency Formula: Check net worth monthly or quarterly. Frequent enough for feedback, spaced enough to capture real progress.

Informed Decision-Making & Planning

Net worth is your financial scoreboard—ignore it and you’re playing blind.

Context for Major Moves

House, Career, Retirement: A single glance at your net worth answers “Can I afford this?” better than any mortgage calculator. If the purchase drags your wealth down or leaves you house‑heavy, pump the brakes.

Goal‑Based Planning

Cash vs. Illiquid: A $50 K net worth mostly in cash? You can peel off $30 K for a down payment and still sleep at night. If that same $50 K lives inside a 401(k) and home equity, you’re asset‑rich, cash‑poor—time to rethink timelines or funding sources.

Debt in Perspective

Ratio Reality Check: A $20 K car loan against a $300 K net worth is a rounding error; against $5 K in assets, it’s a red flag. Keep big‑ticket debt—like your home—within roughly 35 %‑50 % of total net worth to stay balanced, not over‑leveraged.

Investment Performance & Allocation

Umbrella Metric: Your net worth jumps—was it savings, stocks, or selling a side hustle? It sinks—was it a market dip or credit‑card creep? One number tells you when to drill into the details and fix leaks fast.

Preparing for Life Curveballs

Kids, Career Swaps, Emergencies: A rising net‑worth trendline says “green light.” A flat or falling line is your early warning system to save more, invest smarter, or adjust expectations—long before the curveball hits.

Long-Term Progress and The Power of Compounding

Compounding turns time into rocket fuel—track it and watch the launch.

Checkpoints That Matter

Every net‑worth update is a mile marker on the road to independence. Early progress feels like walking in wet cement, but stick with it, and the pace turns into a sprint as compounding kicks in.

Compound Growth in Action

- Yearly Example: Invest $5 K a year at 7 %:

- Age 25–35 → ≈ $70 K

- Age 35–45 → ≈ $210 K

- Age 45–55 → ≈ $460 K

- Notice how the last decade’s growth dwarfs the first—that’s your money earning its own paycheck.

Long‑Term Lens, Short‑Term Calm

Market dip? Job hiccup? A five‑year net‑worth chart reminds you the overall trend is up and to the right. Tracking guards against panic selling and keeps you laser‑focused on the bigger picture.

Celebrate Milestones, Fuel Momentum

- Magic Moment #1: When investment gains outpace new contributions.

- Magic Moment #2: When wiping out a debt instantly boosts monthly cash flow and savings.

These wins prove the system works—log them, savor them, then double down.

Relating Net Worth to Life Goals and Values

Your Personal Freedom Meter

Work‑Optional Threshold: Hit net worth ≈ 25 × annual expenses (the 4 % rule) and you can live off investment income. Track it, and you’ll know exactly how close you are to clocking out—or scaling back—whenever you choose.

Goals in Sharp Focus

- Early Retirement? Your net‑worth chart shows if you’re on pace or need a bigger push.

- Dream Home, Sabbatical, World Tour: Plug each goal’s price tag into your tracker so every update screams “Getting closer!” or “Time to tweak.”

Values‑Driven Decisions

Spend vs. Invest Intentionally: A $5 K luxury vacation that delays your freedom date by six months—worth it? There’s no wrong answer, only deliberate choices aligned with your values.

Legacy & Security

Family and Causes: Funding college, gifting to charity, leaving an inheritance—net‑worth tracking keeps legacy goals measurable and on track. Lagging? Adjust contributions or investment mix now, not later.

Purpose‑Powered Motivation

Numbers alone won’t fire you up—but numbers tied to purpose will. When every $1 saved or invested moves you closer to a life milestone, staying disciplined feels natural.

How to Track Your Net Worth

You can use a notebook, a spreadsheet, or even apps designed to help you track your net worth. Tracking your net worth doesn’t have to be complicated. Here are some simple steps to get started:

Calculate Your Net Worth Once – Today

Using the basics from above, sit down and do that first calculation. List out your assets and liabilities, get the totals, and find out your number. It might be tempting to procrastinate, but remember, knowledge is power. Even if it’s not a number you’re proud of yet, this is your starting point – and everyone starts somewhere.

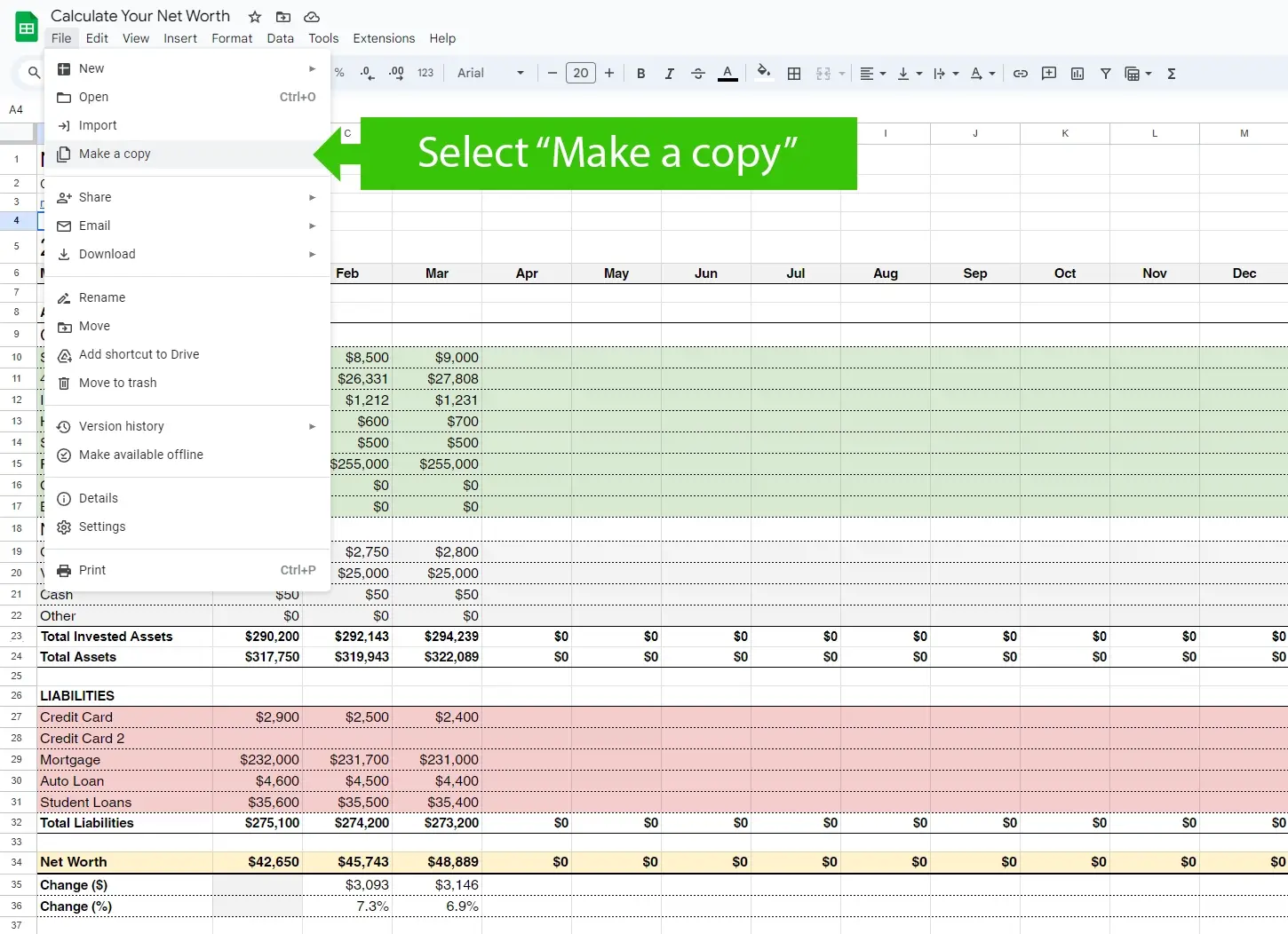

- Quick options: Jot it down on paper, use a simple Excel/Google Sheet, or an online net worth calculator. (We’ve included a free Google Sheet template from Net Worth Insights to make this easy – more on that soon!)

Pro Tip: Save a copy of this initial calculation. This is like a “before” photo in a fitness journey. You’ll want to look back at it later to see how far you’ve come.

Choose a Tracking Method That Works for You

There are a few popular ways to track net worth – pick one that you’ll stick with:

- Spreadsheet (Manual) – Perfect if you like full control. You can use Excel or Google Sheets. You’ll enter account balances and values yourself. It’s simple and customizable (you can add whatever categories or notes you want). Many find the act of entering numbers manually makes them more connected with their money. We’ve got a free Net Worth Insights Google Sheet that’s beginner-friendly and already set up with the formulas – just plug in your numbers each time.

- Automated Apps/Platforms – These connect to your bank and investment accounts and update your net worth automatically. They’re convenient (no manual data entry after the initial setup) and often come with charts and analytics. Examples include Empower (formerly Personal Capital) – a free dashboard that aggregates all accounts.

, or Mint (a popular free budgeting app that also tracks net worth) – though note Mint’s future is evolving as it merges into other Intuit offerings. Other paid options like Kubera or Monarch Money offer sleek interfaces and can handle even complex asset types (crypto, real estate estimates, etc.).

- Hybrid (Spreadsheet + Feeds) – If you want the best of both, tools like Tiller Money provide automated bank feeds into Google Sheets. This means your spreadsheet updates with your latest balances every day, but you still have the flexibility of a spreadsheet format. It’s a great solution for those who love spreadsheets but not manual data entry. (Tiller offers a 30-day free trial, then about $79/year.)

- Decision factor: If you enjoy tech and want real-time updates, an app might be best. If you prefer a hands-on approach and customization, go with a spreadsheet. There’s no wrong choice – the best method is the one you’ll actually use consistently.

Set a Schedule (Consistency is Key)

Decide how often you’ll update and review your net worth. Common frequencies are monthly or quarterly. Monthly is great to stay very tuned-in (and is typical if you’re in a growth or debt-payoff phase and want to see progress each month). Quarterly is fine if your finances are on autopilot and you just want periodic check-ins. Mark it on your calendar or set a reminder. Example: “Net worth review on the 1st of every month.” It can even become something you look forward to – a little ritual of seeing where you stand.

- Avoid tracking too often (like daily or weekly) – investments can swing and bills come at different times, which can make ultra-frequent tracking misleading and stressful. Give enough time for meaningful change between check-ins.

- When you update, record the date and the net worth figure. Over time, you’ll compile a log of data points that you can graph or analyze to truly see your trajectory.

Use Categories and Notes

As you track, it helps to break your net worth into categories. For assets, you might separate “Retirement Accounts,” “Real Estate,” “Cash Savings,” “Investments,” “Personal Property.” For liabilities: “Mortgage,” “Student Loans,” “Credit Cards,” etc. This way, you not only see the total, but also how each part changes. Maybe your investments grew but you bought a car (adding a liability), so one went up and one went down. Noting those changes helps explain why your net worth moved.

- Most apps will automatically categorize by account type, and if you use a spreadsheet, consider creating sections for each category. Our Net Worth Insights template, for example, has predefined sections for common asset and debt categories, which you can customize.

- Add notes for context: Jot a one-liner when something significant happens – “Got a bonus, added to savings,” “Market drop this month, investments down,” “Paid off car loan!” These notes will be gold when you look back. They turn your net worth history into a story of your life events and decisions.

- Avoid tracking too often (like daily or weekly) – investments can swing and bills come at different times, which can make ultra-frequent tracking misleading and stressful. Give enough time for meaningful change between check-ins.

- When you update, record the date and the net worth figure. Over time, you’ll compile a log of data points that you can graph or analyze to truly see your trajectory.

Analyze and Adjust

Every so often (perhaps once a year), take a deeper dive. Look at your net worth trend line. Are you happy with the direction and speed? If yes, great – keep doing what you’re doing. If not, this analysis can spotlight areas to improve:

- Identify Bottlenecks: Maybe your net worth isn’t growing because debt is dragging it down (interest piling up), or maybe you’re sitting on too much cash that’s not invested. Identifying these factors can lead to action (like refinancing expensive debt, or moving cash into investments for growth).

- Revisit Goals: Use your tracking to see if you’re on pace for the goals you set. If you aimed to increase net worth by $10K this year and you’re only up $5K mid-year, you might decide to boost your savings rate or cut an expense to catch up. On the other hand, if you surpassed your goal early, perhaps set a new stretch goal!

- Life Events: Adjust for any life changes. If you get married and merge finances, you’ll have a joint net worth to track. If you buy a house, your asset and liability mix changes – ensure you’re including new entries (house value, mortgage). The tracking process is flexible; update your method as your life evolves (our template allows adding/removing line items easily, and apps will update when you link new accounts).

Stay Motivated – Use Tools & Communities

To avoid “tracking fatigue,” leverage tools that make it fun. Many apps display your net worth in pretty charts or even celebrate milestones (Empower, for example, has graphs that show your progress and can project future net worth). You can also engage with personal finance communities – lots of people share their net worth journeys on blogs or forums, and cheering each other on can be motivating. Consider joining a subreddit or community challenge where you post updates (anonymously if you prefer) to keep yourself accountable.

- Gamify it: Some people set up mini-challenges, like a Net Worth Challenge to increase it by a certain amount in a timeframe, or to hit a net worth equal to a year’s salary by a certain age. These little games, when tracked, can spur you to find creative ways to win (like finding an extra $100 to invest or selling unused items to reduce clutter and boost savings).

Our Two Recommendations

You can track your net worth for free with our free Google spreadsheet. If you are looking for a more automated way to track your net worth, then we recommend downloading Rocket Money for your phone. Rocket Money Premium is the cheapest net worth solution at only 36 dollars a year. (As of July 2024)

Conclusion: Track Your Net Worth Today – Your Future Self Will Thank You

Net‑worth tracking isn’t bookkeeping—it’s the single habit that turns fuzzy dreams into actionable targets. It shows where you stand, fuels motivation, and supplies the data to steer smarter. Whether you’re 20 or 50, today’s number is just a baseline; commit to logging it monthly and the trend will push you to save, invest, and kill debt. Your move: Spend 30 minutes calculating your net worth now (grab our free Net Worth Insights Sheet or an app), set a reminder for next month, and watch twelve check‑ins turn into a clear, upward trajectory. Start today and let every entry move you closer to the life you want.