The Latte Effect vs. Low-Overhead Strategy debate matters because both are trying to answer the same question: where is the easiest place to find money to invest? This article breaks down where the Latte Effect came from, why it became so popular, and why cheaper housing plus a cheaper car usually beats coffee-cutting by a mile when you are young.

The takeaway is not “buy every latte you want.” The takeaway is sharper: small expenses matter, but structural expenses decide the game. If you want to build wealth faster, focus first on the two line items that quietly dominate most budgets: where you live and what you drive.

The Latte Effect: Where It Came From and Why It Got So Much Hype

The Latte Effect, often called the Latte Factor, was popularized by personal finance author David Bach, especially through his book The Automatic Millionaire. The idea is simple: if you cut a small daily purchase, like a $5 latte, and invest that money instead, compounding can turn that tiny habit into serious wealth over time.

The concept became popular because it is easy to understand. Everyone can picture a coffee. Everyone can multiply $5 by 30 days and realize that “just a little treat” may actually be $150 per month. It also gives people a feeling of control. You do not need a promotion, a finance degree, or a six-figure income to skip one purchase and redirect the money.

The hype also came from a real truth: automatic investing works. If someone finds $150 per month and invests it consistently into a low-cost index fund, that can absolutely become meaningful money. The Latte Effect is not mathematically wrong. It is just incomplete.

- Why it caught on: It turns wealth building into a daily decision people can understand.

- Why it feels empowering: It gives immediate action: skip the latte, invest the difference.

- Why it gets criticized: It can make people feel guilty over small joys while ignoring the giant expenses draining thousands per month.

Action step: pull up your last 30 days of transactions and find your “latte category.” It may be coffee, takeout, delivery fees, subscriptions, convenience-store snacks, or impulse Amazon purchases. Do not judge it yet. Just total it.

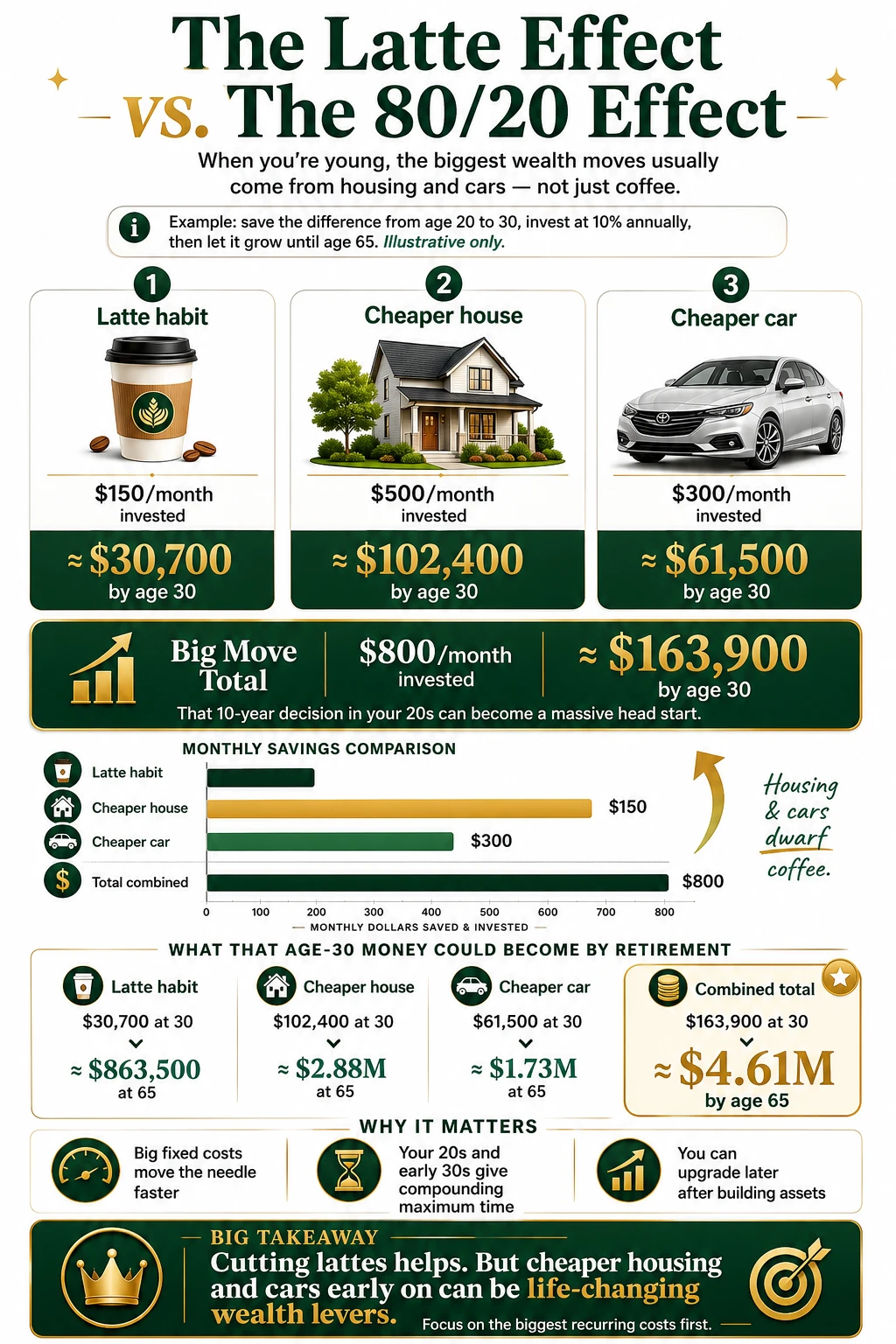

Latte Effect vs. Low-Overhead Strategy: Infographic

Latte Effect vs. Low-Overhead Strategy: The Math Is Not Even Close

The Low-Overhead Strategy focuses on keeping your biggest fixed costs unusually low while you are young, then investing the gap. Instead of asking, “Can I save $6 by skipping coffee?” it asks, “Can I save $600 to $1,500 per month by choosing a cheaper apartment, renting with roommates, buying a modest used car, or staying car-light?”

That difference is massive because monthly investing is a compounding engine. The more dollars you can feed into it early, the more time those dollars have to grow.

In this formula, PMT is the monthly amount invested, r is the monthly return, and n is the number of months. If we assume a 7% average annual return, then the monthly return is about 0.583%. That is not a guarantee; it is simply a reasonable long-term planning assumption often used for diversified stock market investing.

Here is what happens over 10 years when the monthly savings are invested at 7% annually:

- $180 per month from skipping $6 daily coffee: about $31,000.

- $600 per month from cheaper housing or a cheaper car: about $104,000.

- $1,000 per month from lower rent plus a modest vehicle: about $173,000.

- $1,500 per month from aggressive low overhead: about $260,000.

The Latte Effect is not useless. But the Low-Overhead Strategy attacks the real wealth-building lever: monthly investable surplus. Coffee may free up $100 to $200. Housing and transportation can free up four figures.

Why Housing Is the Biggest Low-Overhead Wealth Lever

Housing is usually the largest line item in a young adult’s budget. That makes it the highest-impact place to look for wealth-building margin. A $300 coffee habit gets attention because it is visible, but a $2,400 apartment quietly sets the entire budget on fire if your take-home pay is $4,500.

A strong rule of thumb is to keep housing below 25% to 30% of take-home pay when you are trying to invest aggressively. If you are in an expensive city, that may require tradeoffs: roommates, living farther from downtown, renting instead of buying, house hacking, or choosing a smaller place than your income technically allows.

Consider two 25-year-olds earning the same income:

- Person A rents the luxury one-bedroom: $2,250 per month.

- Person B rents with a roommate: $1,350 per month.

- Monthly difference: $900.

- 10-year invested difference at 7%: roughly $156,000.

That is the point most Latte Effect conversations miss. A housing decision made once can create an automatic investing advantage every single month. You do not need daily willpower. You need a lower fixed expense.

If you are buying, the same logic applies. A starter home or condo with a manageable payment can be wealth-building. Stretching into the maximum mortgage your lender approves can trap you. Lenders approve based on whether you can make the payment, not whether you can also invest, travel, handle emergencies, and sleep well.

- Renters: compare units by total monthly cost, including utilities, parking, pet fees, commuting, and renter’s insurance.

- Buyers: calculate the all-in monthly cost: mortgage, property taxes, insurance, HOA, maintenance, and repairs.

- Young professionals: consider “boring housing” for 3 to 5 years so your investment accounts can become exciting.

Action step: calculate your housing percentage using take-home pay, not gross income. If housing is above 35% of take-home pay, make your next lease or purchase decision a wealth-building decision, not just a lifestyle upgrade.

Why Cars Destroy More Wealth Than Lattes Ever Will

Cars are the second major target of the Low-Overhead Strategy. A new car can feel affordable when the dealership stretches the loan to 72 or 84 months, but the total cost is much larger than the payment. You have depreciation, insurance, registration, repairs, maintenance, fuel, and interest.

According to AAA, the average annual cost of owning a new vehicle in the United States has climbed into five-figure territory when depreciation, financing, maintenance, insurance, fuel, and fees are included. That does not mean no one should own a car. It means the car decision deserves more respect than the coffee decision.

A $700 monthly car payment is not just $700. If the vehicle also increases insurance by $150 per month and costs another $150 more in fuel and maintenance than a modest alternative, the real gap may be $1,000 per month. That is wealth-building rocket fuel if invested instead.

A practical car rule: if you are young and building wealth, aim for a reliable used vehicle where the total transportation cost stays below 10% to 15% of take-home pay. Total transportation means payment, insurance, gas, maintenance, parking, and registration.

- Better car choice: a 5- to 8-year-old Toyota Corolla, Honda Civic, Mazda3, or similar reliable vehicle.

- Risky car choice: a luxury SUV financed for 72 months because “the payment fits.”

- Best case if possible: live close enough to work that you can go car-light, share a vehicle, bike, walk, or use public transit.

Action step: calculate your true monthly car cost. Add payment, insurance, fuel, maintenance, parking, tolls, registration, and depreciation if you can estimate it. If the number shocks you, that is exactly why the Low-Overhead Strategy works.

The Low-Overhead Strategy in 3 Practical Moves

The goal is not deprivation. The goal is to create a lifestyle where investing is easy because your fixed costs are low. Once the big expenses are under control, small pleasures fit without guilt.

Choose Housing That Leaves Room to Invest

Before signing a lease or mortgage, decide your investing target first. For example, if you want to invest 20% of take-home pay, treat that like a non-negotiable bill. Then choose housing that works after that investment comes out.

If your take-home pay is $5,000 per month and you want to invest $1,000, you are really planning your lifestyle around $4,000. That may make a $2,200 apartment obviously too tight. A $1,500 option may feel less glamorous, but it can buy you years of compounding.

Drive the Cheapest Reliable Car Your Ego Can Tolerate

The phrase “your ego can tolerate” matters because many car purchases are emotional status decisions dressed up as practical decisions. Reliability matters. Safety matters. But a huge payment in your 20s can delay investing, home buying, business building, and financial flexibility.

If you already have a high car payment, run the numbers on selling, refinancing, or replacing the vehicle with something less expensive. Do not assume you are stuck. Check private-party value, loan payoff, insurance changes, and transaction costs before making a move.

Automate the Difference Before Lifestyle Creep Finds It

The Low-Overhead Strategy only works if the savings actually get invested. If you choose a cheaper apartment and then spend the difference on restaurants, gadgets, and weekend trips, you did not build wealth; you just moved spending categories.

Set an automatic transfer to a brokerage account, Roth IRA, 401(k), or high-yield savings account depending on your goal. If your cheaper housing saves $700 per month, automate at least $500 to $700. Make the investment happen the day after payday so the money never sits around waiting to be spent.

If you need a simple framework for tracking the impact, start with your net worth and update it monthly. The guide Net Worth Formula walks through the basic calculation.

Where the Latte Effect Still Helps

The Latte Effect has a role, especially for people who need an easy first win. If someone feels overwhelmed by money, saving $5 or $10 per day can build confidence. It can also expose spending patterns that are more expensive than they look.

The problem starts when the Latte Effect becomes the main plan. You can only cut so many small joys before life feels restrictive. Worse, focusing too hard on tiny purchases can distract you from negotiating pay, lowering rent, avoiding car debt, and investing consistently.

✓ Pros

- Easy to understand and start immediately

- Builds awareness around daily spending

- Can create a beginner investing habit

✗ Cons

- Usually produces smaller monthly savings

- Can create guilt around harmless purchases

- Does not fix oversized housing or transportation costs

Use the Latte Effect as a microscope, not the whole strategy. It helps you notice leaks. The Low-Overhead Strategy helps you reroute the river.

- Use Latte Effect thinking for: subscriptions, food delivery, impulse purchases, convenience fees, and habits that do not add much happiness.

- Use Low-Overhead thinking for: rent, mortgage size, car payments, insurance, commuting costs, and lifestyle commitments.

- Best combination: cut the small stuff you do not value, protect the small stuff you do value, and aggressively reduce the big fixed expenses.

Action step: pick one small spending leak to clean up this week, but pick one large fixed expense to improve before your next lease renewal, car purchase, or move.

The Better Wealth Rule: Spend Freely on What Matters, Ruthlessly Lower What Does Not

The strongest personal finance plan is not anti-coffee. It is anti-waste. If a $6 latte with a friend genuinely improves your day, it may be worth keeping. If a $900 higher rent payment only saves you five minutes of commuting and keeps you from investing, that is a much bigger problem.

A useful rule is to divide expenses into three buckets:

- Joy expenses: things you value and can afford, such as coffee dates, hobbies, travel, fitness, or family experiences.

- Utility expenses: things you need but do not emotionally care about, such as insurance, phone plans, internet, basic transportation, and groceries.

- Status expenses: things mostly purchased to signal success, such as luxury apartments, oversized vehicles, designer upgrades, or premium versions you do not truly use.

Keep joy expenses within reason. Optimize utility expenses. Be extremely suspicious of status expenses. Status spending is dangerous because it often becomes fixed: a lease, a car loan, a mortgage, a club membership, or a lifestyle that is hard to unwind.

If you are young, the Low-Overhead Strategy gives you something more valuable than looking rich: options. Options to invest. Options to change careers. Options to start a business. Options to buy assets when markets fall. Options to say no to bad jobs, bad landlords, and bad debt.

Here is the simplest version of the wealth showdown:

- The Latte Effect asks: “What small daily purchase can I cut?”

- The Low-Overhead Strategy asks: “What big monthly obligation can I avoid?”

- The winning move asks: “How much can I automatically invest because my lifestyle is intentionally affordable?”

Start with the big rocks. Choose housing below your maximum. Drive less car than the bank says you can afford. Automate the gap into investments. Then enjoy the latte if it fits the plan.