The Ultimate 80/20 Personal Finance Guide is about finding the few money decisions that drive most of your wealth-building results. If you control the big leaks - housing, cars, debt, lifestyle inflation, subscriptions, and investing automation - you can stop obsessing over daily coffee and start making financial progress that actually compounds.

This guide shows you where the real money goes, how consumer traps quietly steal future income, and how to build a simple system that saves, invests, and protects you with almost zero willpower.

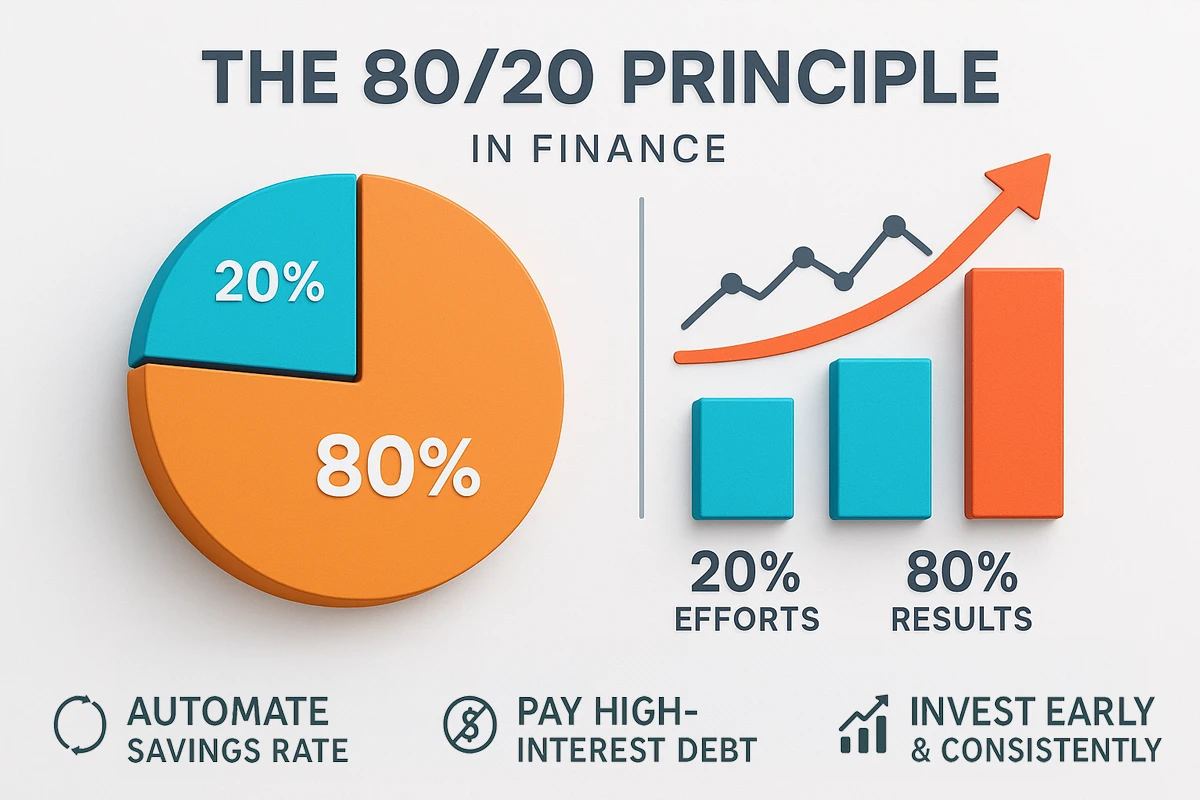

The Ultimate 80/20 Personal Finance Guide Starts With the Big Levers

The 80/20 rule says a small number of inputs often create most of the results. In personal finance, that means your biggest wins usually come from a handful of decisions: how much house you buy, what car you drive, whether you carry credit card debt, how quickly your spending rises with income, and whether your investing happens automatically.

Cutting a $5 coffee five times per week saves about $100 per month. That is not meaningless. But one oversized car payment, one rent decision, or one credit card balance can wipe out years of coffee savings without feeling dramatic in the moment.

- A $750 car payment instead of a $350 used-car payment

- Difference: $400 per month, or $4,800 per year.

- A $2,600 apartment instead of a $2,000 apartment

- Difference: $600 per month, or $7,200 per year.

- A $6,000 credit card balance at 24% APR

- Interest can easily cost $100+ per month before you even reduce the balance.

- Five forgotten subscriptions averaging $18 each

- Difference: $90 per month, or $1,080 per year.

The goal is not to become cheap. The goal is to stop letting low-value spending occupy the same budget as high-value goals. A good personal finance system makes room for the things you genuinely enjoy while aggressively eliminating expenses that do not improve your life.

Your action step: open your last full month of bank and credit card transactions. Ignore tiny categories at first. Circle the five largest recurring costs. Those are the levers that deserve your attention before you start blaming lattes.

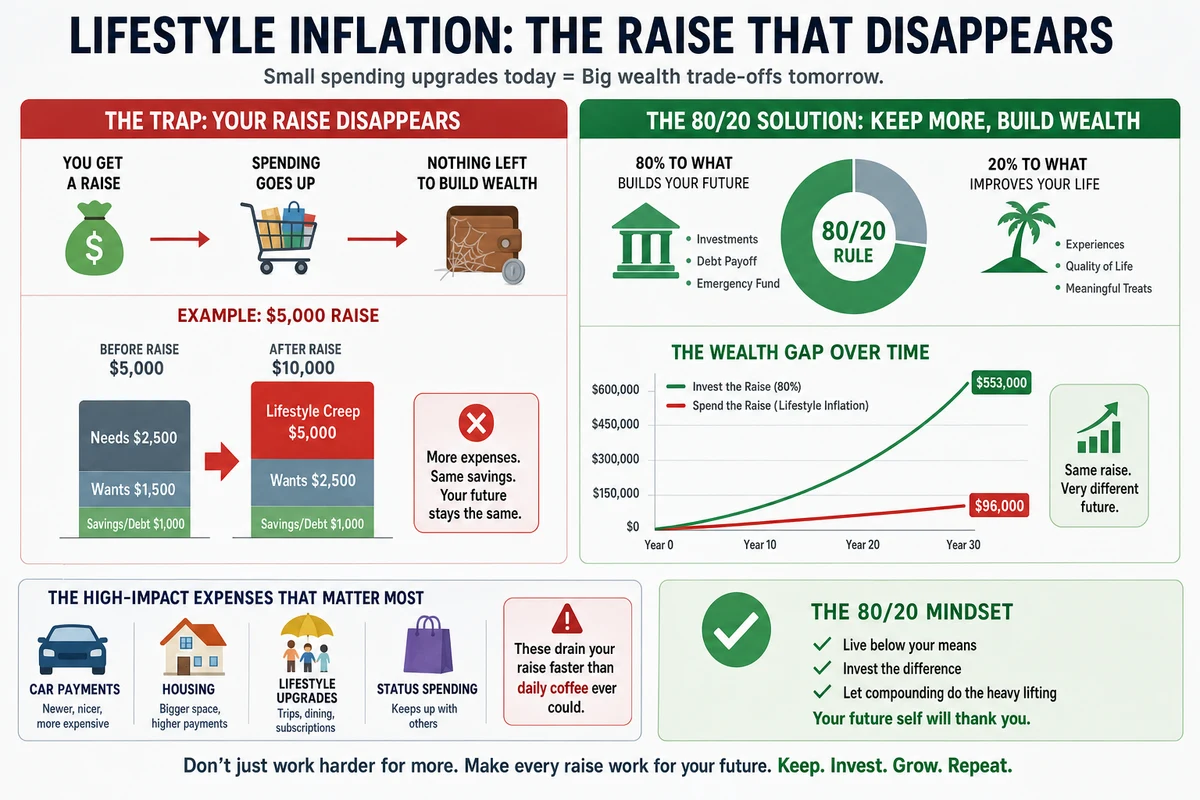

Lifestyle Inflation: The Raise That Disappears

Lifestyle inflation happens when every raise becomes a nicer apartment, bigger home, newer car, pricier restaurants, more travel, better clothes, and extra subscriptions instead of more investing. It feels normal because your income technically supports it - until you realize your savings rate has not improved at all.

The dangerous version of lifestyle inflation is not enjoying your money. It is upgrading automatically. If your income goes from $70,000 to $85,000 and your monthly spending rises by the same amount, your financial life did not improve much. You just gave your future self a more expensive baseline.

Here is a practical example. Suppose a promotion increases your take-home pay by $700 per month. Instead of absorbing the full $700 into restaurants, clothes, car upgrades, and convenience spending, split it:

- $350 to investing

- Increase your 401(k), IRA, brokerage, or automated index fund contribution.

- $150 to lifestyle upgrades

- Enjoy better meals out, hobbies, travel, or personal comfort without guilt.

- $200 to financial cleanup

- Build your emergency fund, pay down debt, or save for a planned purchase.

This is how you build wealth without feeling deprived. You are not freezing your lifestyle forever. You are making sure your savings rate rises when your income rises. That one rule can be worth hundreds of thousands of dollars over a working career.

If you want a simple way to track whether lifestyle inflation is helping or hurting you, measure your net worth every month. Your income can rise and still leave you stuck if your assets are not growing faster than your liabilities.

Credit Card Debt Turns Past Purchases Into Future Pay Cuts

Credit cards are useful payment tools when paid in full. They become wealth killers when balances carry over at 20% to 30% APR. At that point, the problem is not just the old purchase. The problem is that interest turns your past spending into a monthly bill that steals future income.

A $5,000 balance at 24% APR costs roughly 2% per month in interest before fees. That is about $100 in interest in a single month if the balance does not fall. If you only make minimum payments, the payoff timeline can stretch for years.

Using the formula, a $5,000 balance at 24% APR looks like this:

- $5,000 balance

- $5,000 x 24% / 12 = $100 estimated monthly interest.

- $10,000 balance

- $10,000 x 24% / 12 = $200 estimated monthly interest.

That interest payment does not buy groceries, reduce your principal meaningfully, or build an investment account. It is the cost of carrying old consumption forward.

Stop the Bleeding Before Optimizing Rewards

If you carry credit card debt, rewards points should not be the focus. A card that gives you 2% cash back while charging 24% interest is not a win. The first move is to stop adding new balances.

Use a debit card or cash for variable spending until the card is paid off. Keep one card active for autopay bills only if you can pay it in full every month. Then choose a debt payoff method: avalanche for highest interest first, snowball for smallest balance first, or a balance transfer only if you are disciplined enough not to refill the old card.

Your action step: write down every credit card balance, interest rate, and minimum payment. Pay minimums on all cards, then send every extra dollar to the highest APR balance first. Once the first card is paid off, roll that payment into the next one.

The Big Three Consumer Traps: Cars, Buy Now Pay Later, and Subscription Creep

Most people do not ruin their finances with one ridiculous purchase. They get squeezed by several "reasonable" payments that stack together: a car payment, insurance, phone financing, buy now pay later plans, streaming bundles, app subscriptions, delivery memberships, warranties, and gym memberships they barely use.

Audit Your Car Like an Investor, Not a Driver

A luxury vehicle can quietly cost hundreds or thousands per month once you include the payment, insurance, fuel, maintenance, registration, tires, repairs, and depreciation. The payment is only the most visible part.

A $55,000 SUV financed over 72 months at 7% might have a payment near $937 per month. Add higher insurance, premium fuel, maintenance, and depreciation, and the true monthly cost can push well above $1,200. That is mortgage-level money for an asset that usually loses value.

- Car payment rule

- Try to keep your car payment under 10% of monthly take-home pay.

- Total transportation rule

- Keep all transportation costs - payment, insurance, gas, maintenance - under 15% to 20% of take-home pay.

- Financing rule

- Avoid stretching loans to 72 or 84 months just to make the payment feel affordable.

If your car is blocking your ability to invest, build an emergency fund, or pay off high-interest debt, it is not just transportation. It is a wealth transfer from future you to present convenience.

Treat Buy Now, Pay Later Like Debt - Because It Is

Buy now, pay later services from companies like Affirm, Klarna, Afterpay, and PayPal Pay Later make purchases feel smaller by splitting them into installments. A $240 purchase becomes "only $60 today." The problem is that five separate plans can become a hidden debt pile that hits your checking account every week.

The danger is not always interest. Sometimes the bigger danger is confusion. When payments are spread across multiple dates and apps, your budget looks fine until a cluster of installments lands right before rent, utilities, or your credit card due date.

- BNPL rule

- If you would not buy it in full today, do not split it just to make it emotionally easier.

- Stacking rule

- Never have more than one active BNPL plan at a time.

- Budget rule

- Record the full purchase amount immediately, not just the first payment.

Subscription creep works the same way, except the payments repeat until you cancel. Netflix, Hulu, Disney+, Spotify, Apple iCloud, YouTube Premium, Amazon Prime, Peloton, meal delivery passes, software trials, warranty plans, app upgrades, newsletters, gaming services, and "just $9.99" tools can turn into a quiet $200 monthly leak.

Your action step: search your bank and credit card statements for "recurring," "subscription," "membership," "Apple," "Google," "PayPal," and "Amazon." Cancel anything you would not actively sign up for again today.

An Emergency Fund Stops One Bad Month From Becoming a Five-Year Setback

An emergency fund is not boring. It is the financial shock absorber that prevents a car repair, medical bill, job loss, pet emergency, or family crisis from becoming credit card debt. Without cash reserves, even a manageable emergency can trigger a long debt cycle.

The starter target is $1,000 to $2,500 if you are still paying off high-interest debt. That is enough to handle many common emergencies without reaching for a credit card. Once expensive debt is gone, build toward 3 to 6 months of essential expenses. If your income is irregular, your job is unstable, or you support dependents, lean closer to 6 to 12 months.

- Keep it separate

- Use a high-yield savings account at banks like Ally, Capital One, Marcus, or SoFi - not your everyday checking account.

- Define emergencies in advance

- Job loss, urgent repairs, medical needs, and required travel count. Concert tickets, holiday gifts, and routine maintenance do not.

- Refill it automatically

- If you use $600 for a repair, set an automatic transfer until the fund is back to target.

A simple target is to calculate your essential monthly expenses: rent or mortgage, utilities, groceries, insurance, minimum debt payments, transportation, and basic phone/internet. Multiply that number by your target months.

If your essential expenses are $3,500 per month and you want four months of protection, your target is $14,000. That number may feel large, so break it down. At $350 per month, you would reach it in 40 months. At $700 per month, you would reach it in 20 months. Windfalls, tax refunds, bonuses, and sold items can speed it up.

Automate Your Money So Progress Happens With Zero Willpower

The best personal finance system does not require you to feel motivated every Friday. It routes money before you can spend it. Automation works because it turns wealth-building from a repeated decision into a default setting.

Start with payday. The moment income lands, it should already have a job: bills, emergency fund, retirement contributions, debt payoff, investing, and guilt-free spending. If you wait until the end of the month to save what is left, lifestyle inflation and random expenses will usually win.

- Retirement contributions

- Increase your 401(k) or 403(b) contribution by 1% to 2% today if you are not already on track.

- Emergency fund transfer

- Schedule an automatic transfer to savings the day after payday.

- Debt payoff payment

- Set an extra automatic payment toward the highest-interest debt.

- Investment contribution

- Automate deposits into an IRA or taxable brokerage if you have room after essentials and debt strategy.

This is where a simple investment strategy beats constant tinkering. For many long-term investors, a low-cost diversified index fund approach is enough: a total U.S. stock market fund, total international stock market fund, and total bond market fund adjusted for age, risk tolerance, and goals. Vanguard, Fidelity, Schwab, and iShares all offer broad low-cost funds.

The key is not finding the perfect fund. It is investing consistently, keeping fees low, staying diversified, and giving compounding enough time to work. A person who invests $500 per month for 30 years at a hypothetical 7% annual return could end with roughly $610,000. Waiting ten years and then investing the same amount for 20 years could leave them with about $262,000. Time matters more than cleverness.

Your action step: set up one automatic transfer before you finish reading. Even $50 per paycheck matters because it builds the habit and creates a path you can increase later.

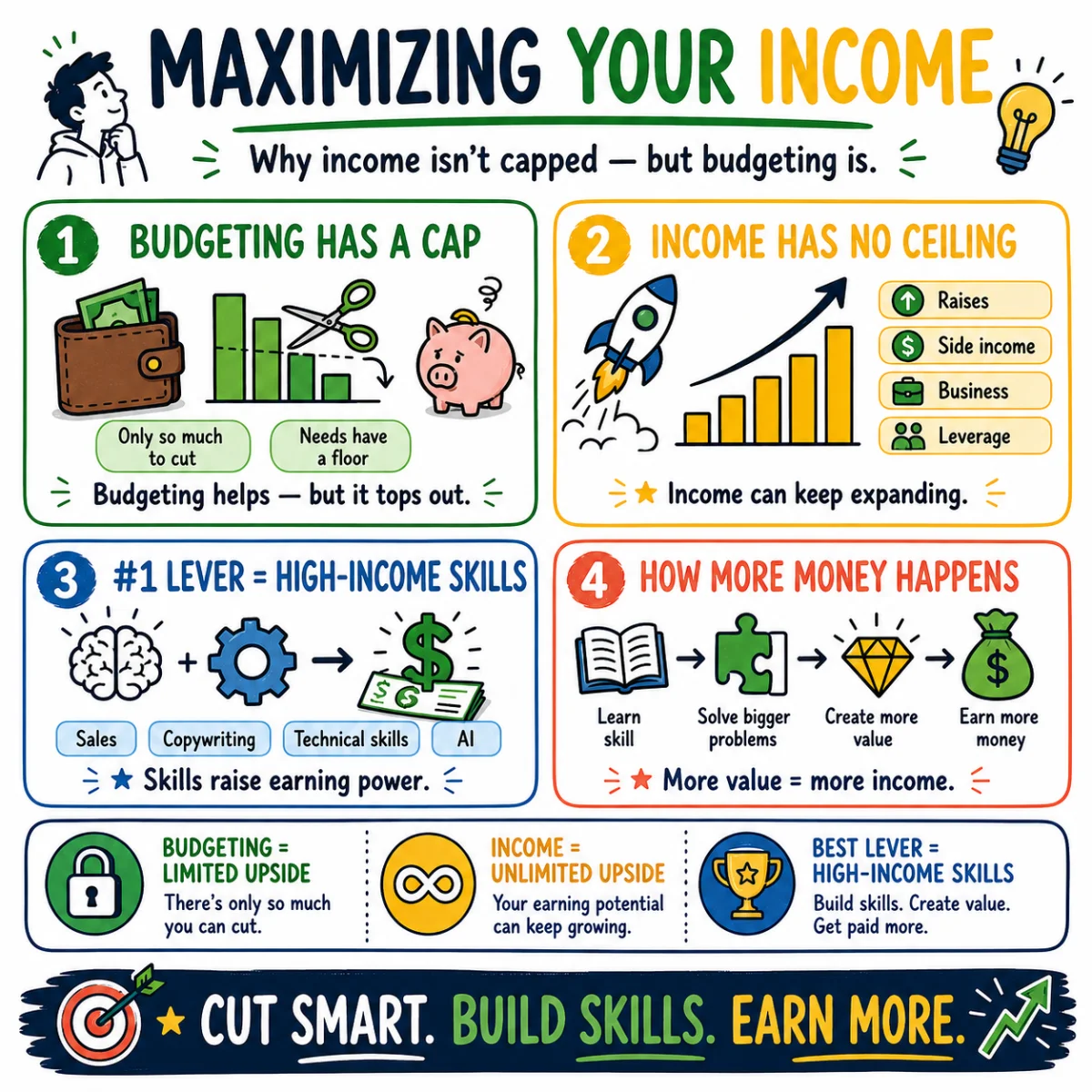

Why Income Beats Extreme Penny-Pinching

Expense control matters, especially on the big categories. But there is a ceiling to how much you can cut. There is no fixed ceiling on income. The strongest 80/20 personal finance move is to pair controlled lifestyle growth with a serious income strategy.

If you save $150 per month by canceling subscriptions and optimizing groceries, that is useful. If you negotiate a $7,000 raise, switch jobs for a $15,000 increase, freelance for $500 per month, or build a skill that changes your earning power, the impact can be much larger.

- Negotiate compensation

- Use salary data from Levels.fyi, Glassdoor, Payscale, or the U.S. Bureau of Labor Statistics before annual reviews.

- Switch roles strategically

- Many people earn their largest raises by changing employers, especially when their current company anchors them to old pay bands.

- Build marketable skills

- Sales, analytics, coding, project management, operations, design, healthcare certifications, and trade skills can directly raise income.

- Create a side income stream

- Freelancing, consulting, tutoring, bookkeeping, local services, and digital products can accelerate debt payoff or investing.

The trick is to protect the new income from lifestyle inflation. If a new job increases take-home pay by $1,000 per month and you invest $600 of it, you have changed your financial trajectory. If you immediately add a $600 car payment, you have mostly changed your driveway.

A good target is to push your savings and investing rate toward 15% to 25% of gross income over time. If you are starting from 0%, begin with 1% and increase every raise. If you are paying off high-interest debt, count extra debt payments as part of your wealth-building rate because they improve your future cash flow.

Your 80/20 Personal Finance Action Plan

You do not need a 40-tab spreadsheet to build wealth. You need a short list of high-impact moves that protect your cash flow, eliminate expensive debt, automate investing, and keep lifestyle inflation under control.

- List your five biggest monthly expenses

- Housing, transportation, debt payments, food, childcare, insurance, and subscriptions are usually where the money is.

- Freeze lifestyle inflation for 90 days

- Do not upgrade housing, cars, restaurants, subscriptions, or recurring expenses while you build your system.

- Attack credit card debt first

- High-interest debt is an emergency because it compounds against you.

- Review your car cost honestly

- If transportation is crowding out investing or savings, consider refinancing, selling, downsizing, or driving the current car longer.

- Cancel low-value recurring charges

- Subscriptions should earn their place every month.

- Build an emergency fund

- Start with $1,000 to $2,500, then work toward 3 to 6 months of essential expenses.

- Automate saving and investing

- Make the transfer happen on payday, before money reaches your spending account.

- Increase income intentionally

- Pick one income move this quarter: negotiate, apply, learn a skill, or launch a small side offer.

The point of the 80/20 approach is freedom from financial noise. You can still buy coffee, go out with friends, travel, and enjoy your money. Just do not let consumer traps quietly consume the dollars that should be building your net worth.

Start with one high-impact move today: cancel one recurring charge, increase your investment contribution by 1%, schedule an emergency fund transfer, or make an extra credit card payment. Small actions matter most when they are attached to the few financial levers that actually move your life forward.