Building a strong savings habit isn't just about setting aside money; it's about understanding the psychology behind saving and implementing strategies that make it easier to stick to your goals. In this post, we'll explore the powerful psychological forces that work against saving—and how to use that same psychology to finally make saving stick.

Understanding the Psychology of Savings

Effective saving is as much about mindset as it is about money. Your brain wasn't wired for long-term financial planning—it evolved to prioritize immediate rewards and avoid short-term pain. That biological mismatch is the root cause of most savings failures. Understanding the specific cognitive biases at play is the first step toward outsmarting them. For a deeper look at how your money beliefs shape your behavior, see The Psychology of Money: A Woman's Guide To Overcoming Financial Anxiety.

Why People Don't Save: The Real Psychological Barriers

Most personal finance advice treats saving as a math problem. It isn't. If it were, everyone who understood compound interest would be wealthy. The real blockers are psychological, and they're deeply wired into how the human brain operates.

Present Bias: Why Tomorrow Never Comes

Present bias is the tendency to overvalue rewards that are available right now and deeply discount future rewards. In a famous experiment, most people would rather have $50 today than $100 in a year—even though a 100% return in twelve months is an extraordinary investment. Your future self feels like a stranger, and your brain treats their financial needs accordingly.

This is why "I'll start saving next month" is such a persistent trap. Next month's you feels abstract and far away. Today's purchase feels real and satisfying. Until you create systems that remove the choice from the moment, present bias wins almost every time.

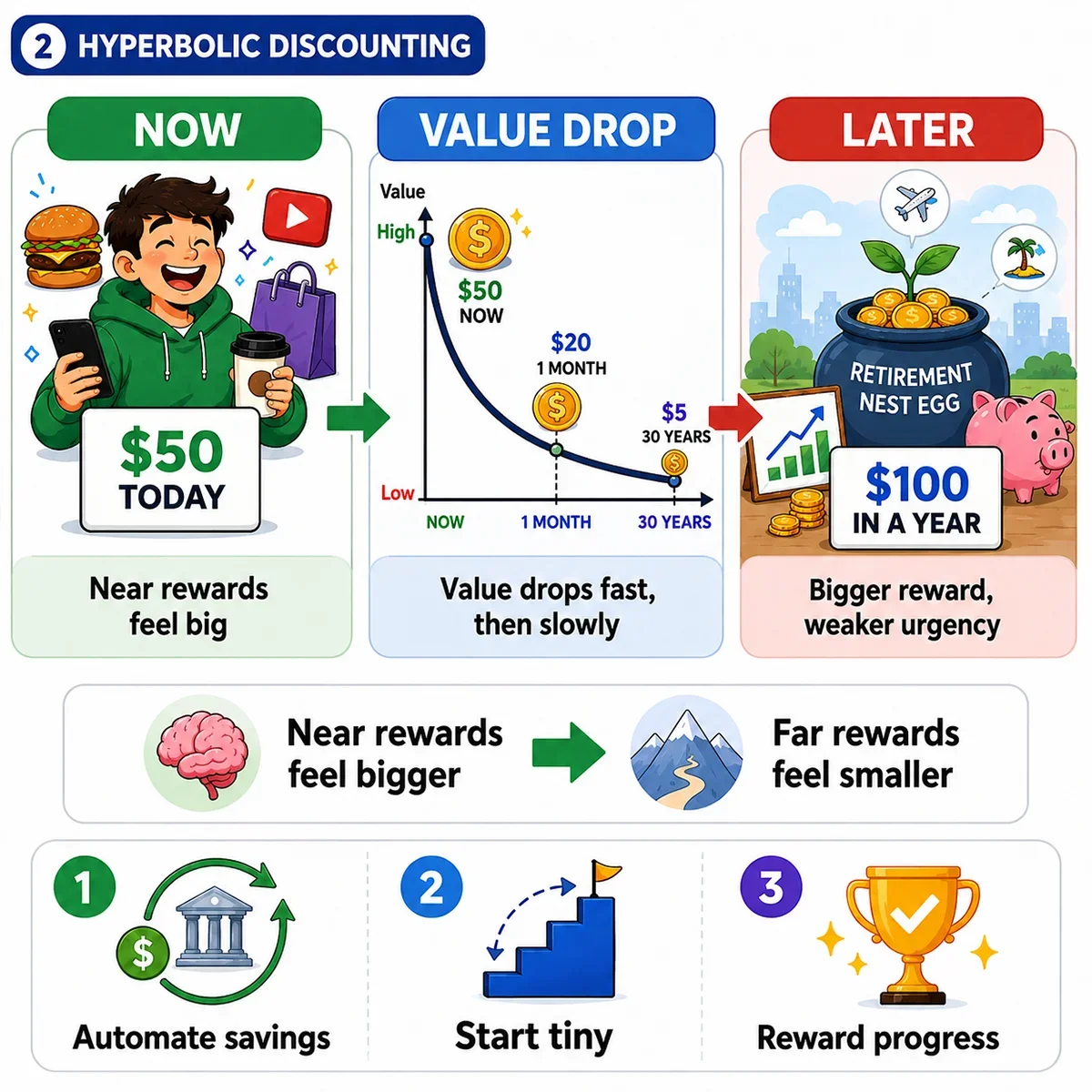

Hyperbolic Discounting: The Shrinking Value of Future Money

Related to present bias, hyperbolic discounting means we don't value future money in a straight line—we discount it steeply at first, then less so over time. The difference between "now" and "one month from now" feels enormous. The difference between "29 months from now" and "30 months from now" feels trivial, even though they're the same gap. This warped perception of time makes saving for retirement especially difficult: decades away feels meaningless, so the urgency never materializes.

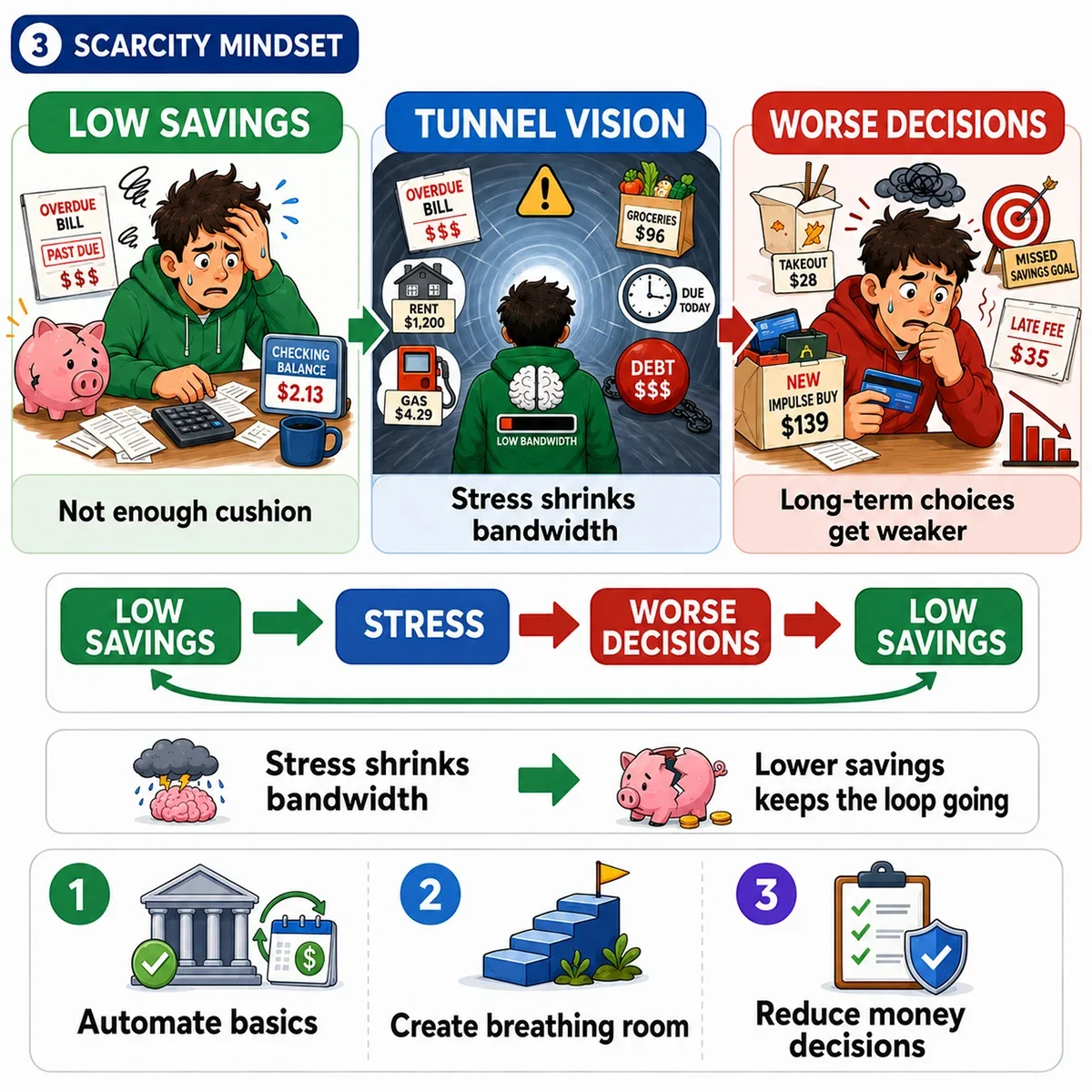

The Scarcity Mindset: When "Not Enough" Becomes a Loop

Research by behavioral economists Sendhil Mullainathan and Eldar Shafir found that scarcity—whether of money, time, or attention—consumes cognitive bandwidth. When you're stressed about money, your mental focus narrows to the immediate crisis. Long-term planning, self-control, and wise decision-making all degrade. This creates a cruel feedback loop: low savings produce financial stress, which impairs the judgment needed to improve savings, which keeps savings low.

This isn't a character flaw. It's a documented cognitive effect. Breaking out of it requires reducing the number of in-the-moment decisions your system depends on. Shifting from a scarcity mindset to a strategy-first approach is explored further in Changing Your Money Mindset - From Scarcity To Strategy.

Social Comparison: Keeping Up Costs More Than You Think

Humans are intensely social creatures, and we calibrate our spending against those around us. When your peer group upgrades their cars, renovates their kitchens, and takes luxury vacations—and broadcasts it all on social media—your reference point for "normal" spending shifts upward, often without you noticing. Lifestyle inflation driven by social comparison is one of the most silent destroyers of savings rates, because it never feels like overspending; it feels like keeping up. Learn how to break this pattern in Law 13 — Avoid Lifestyle Inflation.

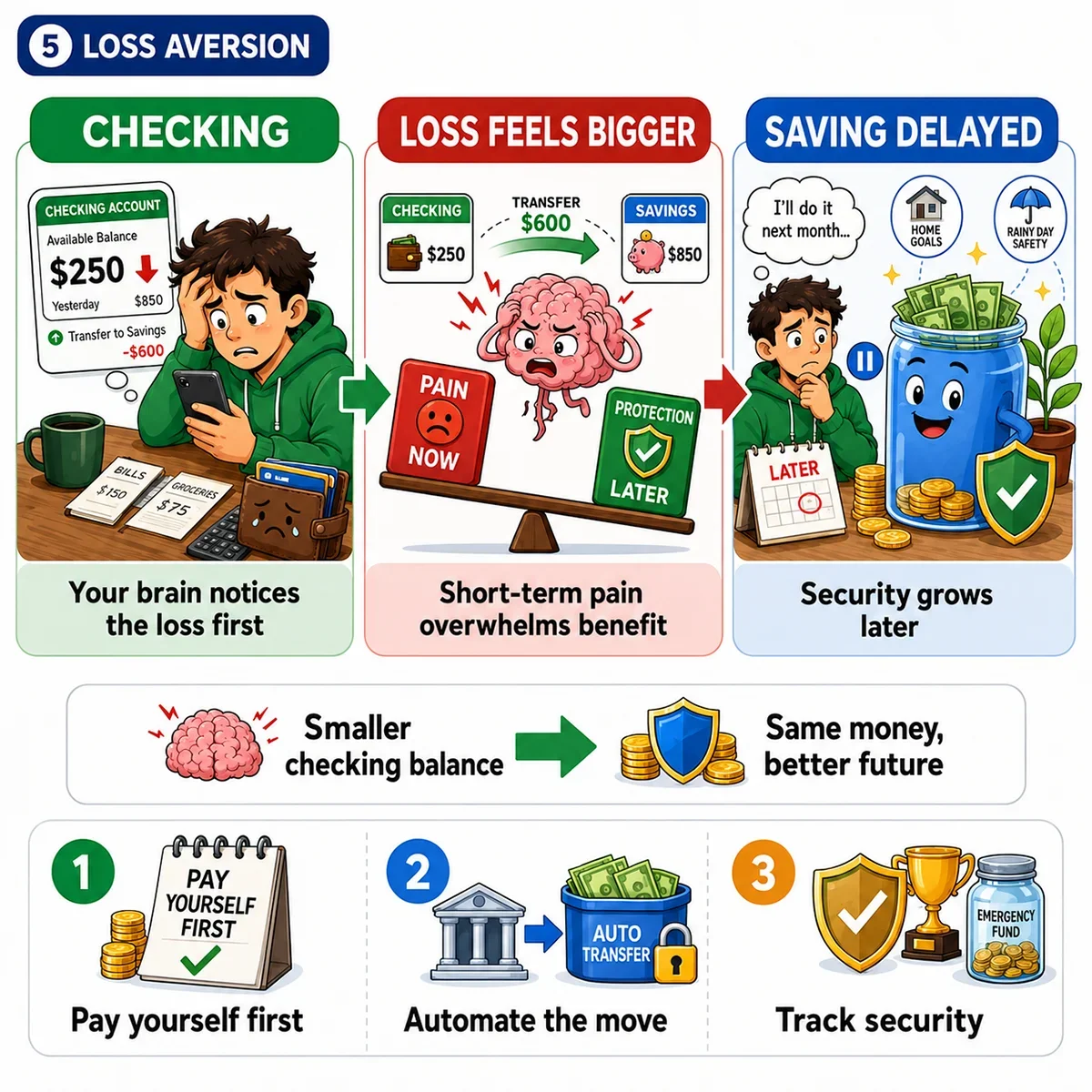

Loss Aversion: Saving Feels Like Losing

Nobel Prize-winning psychologist Daniel Kahneman established that losses feel roughly twice as painful as equivalent gains feel good. Moving money from your checking account to savings feels like a loss, even though it's a gain in disguise. Your brain registers the smaller checking balance as deprivation, triggering discomfort that pushes back against the behavior. This is why willpower-based saving approaches fail: you're fighting a neurological reflex, not just a habit.

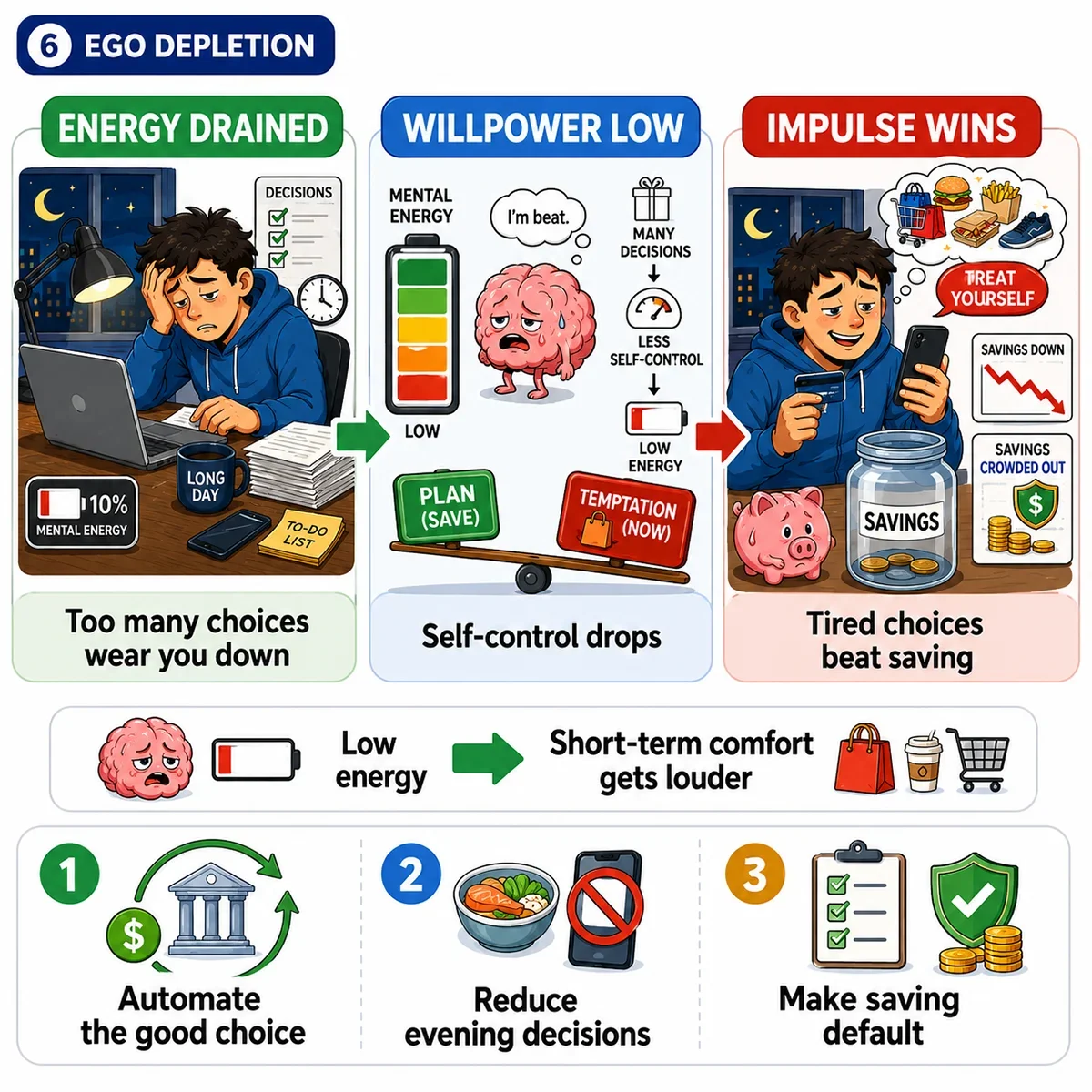

Ego Depletion: Decision Fatigue Sabotages Willpower

Every choice you make throughout the day draws from a finite pool of mental energy. By the time evening arrives—after dozens of work decisions, social interactions, and daily logistics—your capacity for self-control is genuinely depleted. This is when impulsive online shopping, takeout orders, and "treat yourself" purchases happen. Willpower is a resource that runs out, which is why any savings system that depends on it every day will eventually fail.

Automatic Savings: Set It and Forget It

Now that you understand why your brain resists saving, you can design around those weaknesses instead of fighting them. Automation is the single most powerful tool in behavioral finance—it bypasses present bias, sidesteps ego depletion, and converts saving from a repeated act of willpower into a one-time system decision.

Automate Your Savings

Automatic savings is one of the most effective strategies to ensure consistent saving. By setting up automatic transfers from your checking account to a savings account, you remove the temptation to spend that money. Most banks allow you to schedule regular transfers, making saving effortless. Crucially, it also counters loss aversion: when the transfer happens automatically before you see the money, you never feel the "loss" of moving it.

Choose the Right Accounts

Consider using high-yield savings accounts or certificates of deposit (CDs) for your automated savings. These options not only keep your money out of immediate reach but also allow it to grow over time with compound interest.

Review and Adjust Regularly

Set a reminder to review your savings plan every few months. Ensure that the amount you're saving is still aligned with your financial goals and adjust if necessary. As your income increases, consider increasing your savings rate incrementally. For a full breakdown of why this number matters so much, read Why Savings Rate Is Important for Financial Freedom.

Mental Accounting: The Power of Purposeful Money

Mental accounting involves categorizing your money for specific purposes. This psychological strategy can help you visualize your savings goals and stay motivated. For example, by labeling accounts as "Vacation Fund" or "Emergency Savings," you create a clear picture of what you're working towards. It also works with your brain's natural tendency to treat money in different "buckets" differently—money earmarked for an emergency fund is far less likely to be raided for an impulse purchase than money sitting in a general account. If you haven't built your emergency bucket yet, start with Emergency Fund 101: Your Financial Safety Net (Because Life Happens).

Creating a Savings Plan: Steps to Success

Define Clear Goals

Start by defining what you're saving for. This could be an emergency fund, a down payment on a house, or a dream vacation. Clear goals help you stay focused and motivated.

Break Down Goals Into Milestones

Divide your big goals into smaller, manageable milestones. For instance, if your goal is to save $20,000 for a car, aim for $5,000 increments. Achieving these smaller milestones provides a sense of accomplishment and keeps you motivated.

Overcoming Psychological Barriers

Knowing the barrier is half the battle. Here's how to directly counter each one:

- Against present bias: Use implementation intentions—instead of "I'll save more," decide exactly when, how much, and which account. Specificity dramatically increases follow-through. Pair future savings with something enjoyable now (e.g., a small reward after setting up auto-transfer).

- Against hyperbolic discounting: Make your future self vivid. Some research shows that viewing age-progressed photos of yourself increases retirement savings contributions. Write a letter to your 65-year-old self. Name your savings accounts after the specific goal.

- Against the scarcity mindset: Reduce financial decision load. Automate and simplify. Even small wins—saving $25 a week—break the scarcity loop by proving you can accumulate, which shifts your mental model.

- Against social comparison: Audit your information diet. Unfollow accounts that trigger lifestyle envy. Remind yourself that social media is a highlight reel—many people projecting wealth are carrying significant debt to fund it.

- Against loss aversion: Reframe saving as "paying yourself first." Instead of feeling like you're losing access to money, frame each transfer as the most important bill you pay—to your future financial freedom.

- Against ego depletion: Schedule financial decisions in the morning. Never make savings changes when you're tired, hungry, or emotionally stressed. Build your system once, on a good day, so it runs on autopilot every day.

Leveraging Financial Tools

Utilize financial tools like budgeting apps and savings calculators to track your progress. These tools provide a visual representation of your financial journey and help you stay accountable.

Putting It All Together

By combining automatic savings with mental accounting, you create a powerful framework for building and maintaining a strong savings habit. Remember, the key is consistency and adaptability. As your financial situation evolves, so should your savings strategies.

Ultimately, understanding the psychology behind saving and employing these strategies can transform your financial landscape, setting you on the path to wealth accumulation and financial peace.