To minimize estate taxes, you first need to know whether your estate is actually exposed, how large the potential tax bill could be, and which moves reduce taxes without giving up too much control. This guide walks through the math, the major planning tools, and the decision rules that help more of your wealth reach the people and causes you choose.

How to Minimize Estate Taxes: Start by Estimating the Taxable Estate

Federal estate tax does not apply to every estate. It generally applies only to the value above the available federal estate and gift tax exemption, after allowable deductions such as debts, administration expenses, charitable bequests, and the marital deduction.

Federal limits are indexed and can change by law, so confirm the current IRS figures before making gifts or filing an estate tax return. For reference, the 2025 federal estate and gift tax exemption was $13.99 million per person, and the annual gift tax exclusion was $19,000 per recipient. Married couples can often combine exemptions, but portability must be handled correctly.

Example: a married couple has a $34 million gross estate, $2 million of deductible debts and charitable bequests, and $27.98 million of combined federal exemption based on 2025 figures. Their estimated taxable estate is $4.02 million. At a rough top-rate estimate of 40%, the projected federal estate tax exposure is about $1.6 million.

Action step: update your balance sheet first. If you have not done that recently, calculate your net worth and include assets that are easy to miss: business interests, real estate equity, retirement accounts, taxable investments, valuable collectibles, and life insurance you personally own.

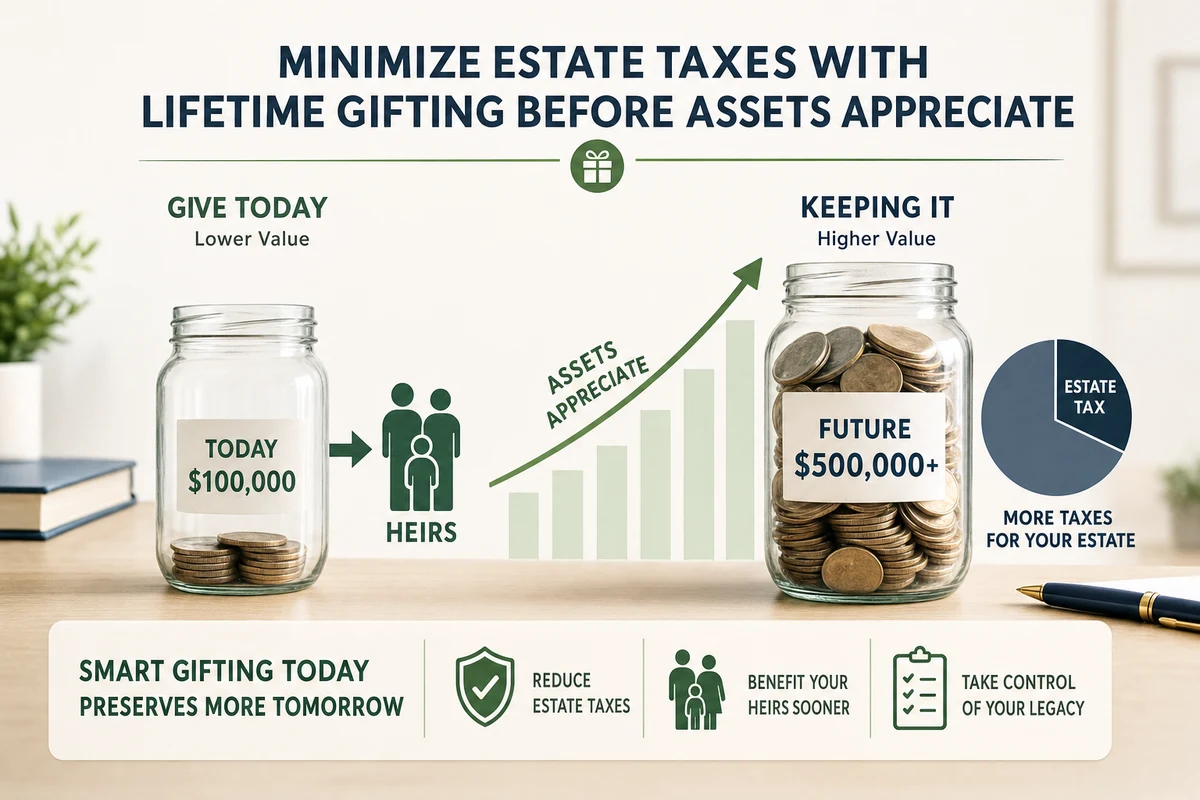

Minimize Estate Taxes With Lifetime Gifting Before Assets Appreciate

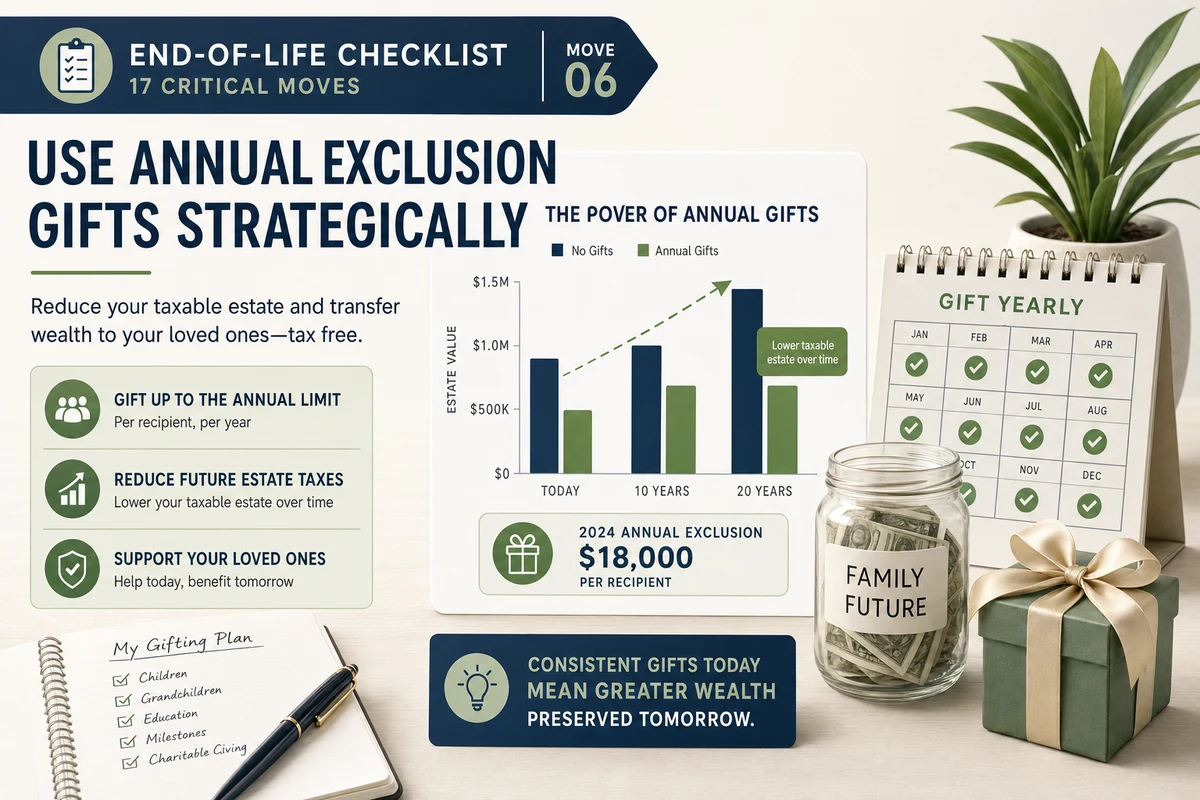

Use Annual Exclusion Gifts Strategically

The annual gift tax exclusion lets you give up to the annual limit per recipient without using your lifetime exemption. Using the 2025 limit as an example, a married couple with three adult children and six grandchildren could give $19,000 × 2 spouses × 9 recipients = $342,000 in one year without reducing their lifetime exemption, assuming the gifts qualify.

This works best when the gifted assets are likely to appreciate. If you transfer shares of a family business, marketable securities, or real estate interests before major growth, the future appreciation can occur outside your estate.

- Best use: families with excess cash flow or appreciating assets they can afford to give away.

- Watch out: gifted assets usually carry over your tax basis, so heirs may lose the step-up in basis they would have received at death.

- Do next: identify recipients, dollar limits, and whether each gift should be cash, investment shares, 529 contributions, or trust funding.

Pay Tuition and Medical Costs Directly

Payments made directly to a school for tuition or directly to a medical provider for qualifying medical expenses generally do not count as taxable gifts. This can be powerful for grandparents who want to help family members without using annual exclusion amounts or lifetime exemption.

A 529 plan can also be “front-loaded” using a five-year gift tax election. Using the 2025 annual exclusion amount, one person could contribute up to $95,000 to a beneficiary’s 529 plan at once, or a married couple could contribute up to $190,000, if they make the proper election and do not make additional taxable gifts to that beneficiary during the five-year period.

Use Trusts to Reduce Estate Taxes Without Losing the Whole Plan

Know Which Trusts Actually Reduce Estate Taxes

A revocable living trust can be useful for probate avoidance, privacy, and continuity if you become incapacitated. But by itself, it usually does not remove assets from your taxable estate because you still control the assets.

An irrevocable trust is different. If structured and administered correctly, it can move assets and future appreciation outside your estate. Common estate-tax-oriented tools include irrevocable gift trusts, spousal lifetime access trusts, grantor retained annuity trusts, and dynasty trusts.

- Best use: assets expected to appreciate significantly, such as private company shares or concentrated investment positions.

- Tradeoff: you usually give up direct ownership and flexibility.

- Do next: ask an estate attorney to model control, access, tax impact, and beneficiary protections before transferring assets.

Use Portability and Marital Planning Correctly

For married couples, leaving everything to a surviving U.S. citizen spouse may defer estate tax because of the unlimited marital deduction. But deferral is not the same as elimination. The surviving spouse may later have an estate large enough to owe tax.

Portability allows a surviving spouse to use a deceased spouse’s unused federal exemption, but it generally requires filing a federal estate tax return after the first spouse dies, even if no estate tax is due. In larger estates, a credit shelter trust or QTIP trust may provide more control and protection than relying on portability alone.

Life Insurance Can Fund Estate Taxes If It Is Owned Correctly

Consider an Irrevocable Life Insurance Trust

Life insurance proceeds are generally income-tax-free to beneficiaries, but they can still be included in your taxable estate if you own the policy or retain certain control rights. That can create a frustrating result: the policy intended to help heirs pay estate tax may increase the estate tax bill.

An irrevocable life insurance trust, often called an ILIT, can own the policy so the death benefit is outside your estate. The trustee can then use the proceeds to provide liquidity to heirs, buy assets from the estate, or lend money to the estate so taxes and expenses can be paid without a forced sale of a business or property.

Example: if a taxable estate includes a $5 million life insurance policy owned personally by the insured, that policy could add up to roughly $2 million of federal estate tax exposure at a 40% top-rate estimate. If an ILIT owns the policy properly, that death benefit may be kept outside the taxable estate.

Family Limited Partnerships Can Help, But Only With Real Substance

Family limited partnerships and family LLCs can transfer business, real estate, or investment interests to family members while allowing senior family members to retain management control. They may also support valuation discounts for lack of control and lack of marketability, which can reduce the taxable value of transferred interests.

For example, a parent might transfer minority non-voting interests in a family real estate LLC to children or trusts. Because those interests cannot easily be sold and do not control the entity, a qualified appraiser may apply a valuation discount. That discount can allow more economic value to move using less gift and estate tax exemption.

- Best use: operating businesses, rental real estate portfolios, or family investment entities with a legitimate business purpose.

- Watch out: the IRS may challenge aggressive discounts, poorly documented transfers, or entities that exist only to avoid tax.

- Do next: document the business purpose, keep proper books, use independent appraisals, and avoid treating partnership assets like personal checking accounts.

Charitable Giving Can Reduce Estate Taxes and Support Your Values

Charitable bequests can reduce the taxable estate dollar for dollar because qualifying charitable gifts are generally deductible for estate tax purposes. The simplest version is naming a charity in your will, trust, retirement account beneficiary form, or donor-advised fund succession plan.

More advanced strategies can combine tax reduction with income planning:

- Charitable remainder trust: can provide income to you or other beneficiaries for a period of time, with the remainder going to charity.

- Charitable lead trust: provides income to charity first, then passes remaining assets to family members later.

- Donor-advised fund: simplifies charitable giving and can create a clear plan for grants after death.

- Private foundation: offers more control but requires more administration, compliance, and cost.

Action step: decide whether your priority is maximum family inheritance, charitable impact, or a blend of both. The right structure depends on that answer.

Retirement Accounts Require Separate Tax Planning

Review Beneficiaries and Roth Conversion Opportunities

Traditional IRAs and 401(k)s can create two tax issues: they may be included in your estate for estate tax purposes, and heirs may owe income tax when they withdraw the money. Under current inherited retirement account rules, many non-spouse beneficiaries must empty inherited accounts within 10 years, which can push withdrawals into high-income years.

Roth conversions can help in the right situation because you pay income tax during your lifetime, potentially reducing the taxable estate and leaving heirs an asset that may be income-tax-free if Roth rules are satisfied. But a Roth conversion is not automatically smart. If your estate is below estate tax thresholds, or if the conversion pushes you into an unnecessarily high tax bracket, the math may not work.

For a deeper comparison, consider the tradeoffs between pre-tax and Roth retirement accounts when planning for estate taxes.

- Do next: confirm every beneficiary form matches your estate plan.

- Check: whether trusts named as IRA beneficiaries are drafted for current inherited IRA rules.

- Model: partial Roth conversions over several years instead of one large conversion in a single high-tax year.

Review Your Estate Plan Before Tax Law or Family Changes Force It

Estate tax planning is not a one-time document signing. Review your plan at least every 2 to 3 years, and sooner after a major life event: marriage, divorce, birth, death, business sale, large inheritance, relocation to a new state, or a major change in tax law.

Use this quick checklist:

- Update asset values: real estate, businesses, brokerage accounts, retirement accounts, insurance, and liabilities.

- Confirm exemptions: federal estate tax exemption, annual gift exclusion, state estate tax rules, and portability status.

- Audit ownership: which assets are personal, joint, trust-owned, business-owned, or beneficiary-designated.

- Check liquidity: whether heirs could pay taxes and expenses without selling key assets under pressure.

- Coordinate advisors: estate attorney, CPA, financial planner, insurance specialist, and business valuation professional when needed.

The practical goal is simple: calculate your exposure, choose the few strategies that fit your family, and execute them before appreciation, tax law changes, or probate problems limit your options.