Delayed gratification in personal finance means choosing a stronger future over a smaller immediate reward. It shows up when you skip an impulse buy, keep investing during volatility, or wait long enough for compound growth to do the heavy lifting. The people who build wealth consistently are not always the highest earners. They are often the people who repeatedly choose long-term value over short-term relief.

That matters because nearly every money decision has an opportunity cost. A purchase is never just the sticker price. It is also the savings, investing, debt payoff, or financial flexibility you give up by spending that cash today.

What Delayed Gratification Means in Finance

Delayed gratification is the ability to resist an immediate reward in favor of a later and larger benefit. In money terms, that can mean contributing to your Roth IRA before upgrading your car, building an emergency fund before booking a luxury trip, or staying invested instead of panic-selling after a market drop.

This skill matters because wealth building is rarely dramatic. It is usually the result of ordinary decisions repeated for years: spending less than you earn, avoiding lifestyle inflation, investing automatically, and giving your money time to compound.

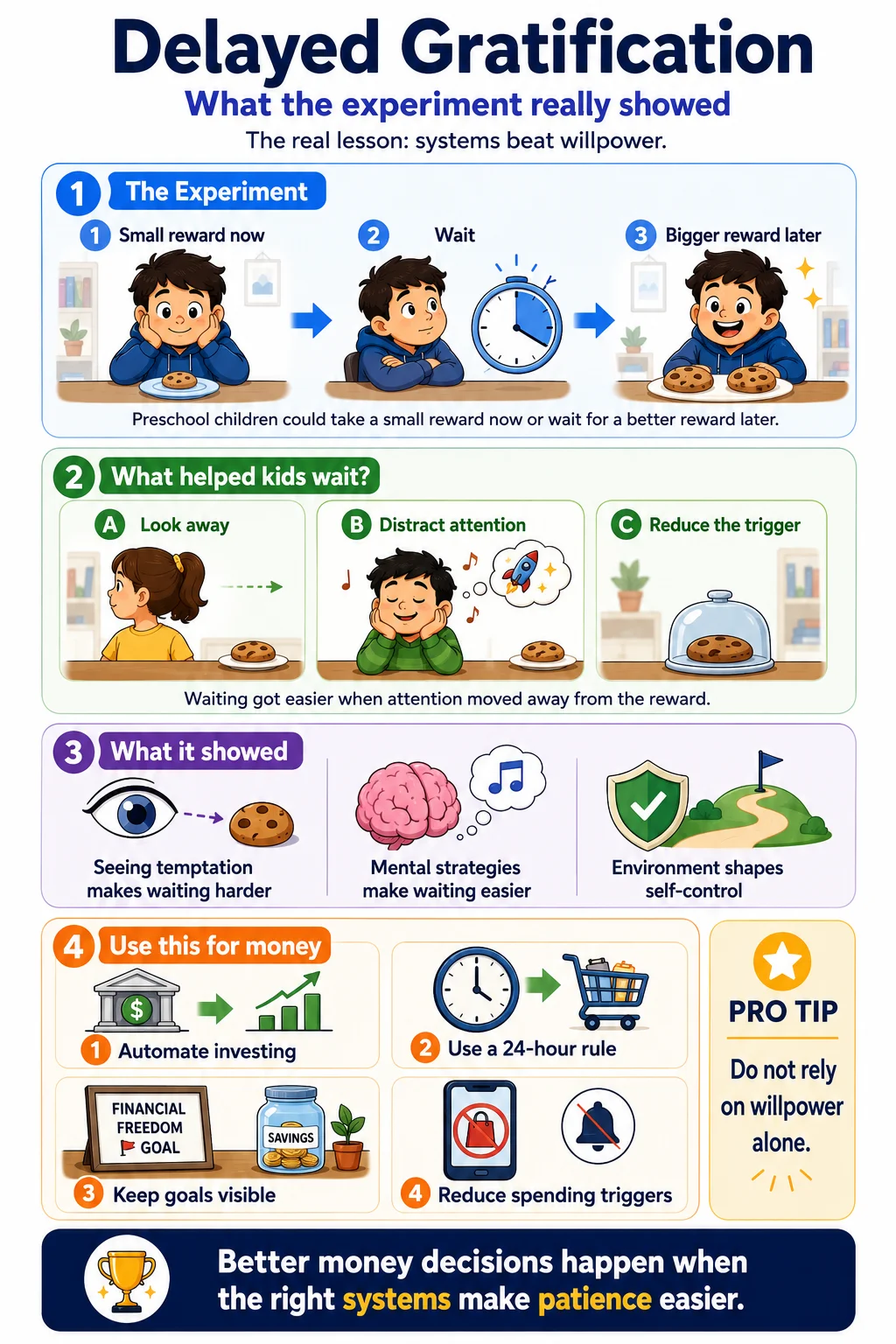

The Science Behind Delayed Gratification

Studies such as the Stanford marshmallow experiment made delayed gratification famous, but the more useful takeaway is not that some people are simply better at self-control. Environment, systems, and habits matter. It is much easier to make patient money decisions when your savings are automated, your goals are visible, and your biggest spending triggers are reduced.

Delayed Gratification and Investment Decisions

Investing rewards patience. Delayed gratification helps you keep buying through boring months, ignore hype cycles, and avoid turning a long-term plan into a series of emotional reactions. By resisting the urge to chase quick wins or bail out during volatility, you give compounding a chance to work.

Every purchase has a hidden price tag: the future wealth you give up by spending instead of investing. Before you buy, ask yourself: if I invested this amount instead, what could it become over the next 10, 20, or 30 years? That simple question turns spending into a direct comparison between today's convenience and tomorrow's freedom.

Opportunity Cost Calculator

What if you invested that money instead?

$1,754

$100 grows to $1,754 in 30 years — a 17.5× gain (+$1,654) at 10.0% avg. annual return (US Large-Cap (S&P 500), 1928–2025).

Disclaimer: These projections are based on historical averages and are for illustrative purposes only. Past performance does not guarantee future results. Actual returns will vary and may be significantly lower, higher, or negative.

Try it with your next impulse buy, subscription upgrade, or lifestyle purchase. The default uses the S&P 500, but you can switch asset classes to compare how different long-term return assumptions change the trade-off. If you want a spending framework to pair with this, start with the 50/30/20 budgeting method and track how much of your income is still available to invest.

How to Think About Every Purchase

Use a quick decision filter before you spend. The goal is not to remove all enjoyment from life. It is to make sure your spending is intentional instead of automatic.

- Ask what problem the purchase solves: Is it meeting a real need, or just reducing boredom, stress, or social pressure for a few hours?

- Calculate the full cost: Include taxes, fees, accessories, maintenance, and any recurring subscription attached to the purchase.

- Compare it to your biggest goal: What goal is this money not funding if you spend it now: debt payoff, investing, an emergency fund, or financial independence?

- Add a waiting period: Give non-essential purchases 24 to 72 hours before buying. Urgency usually fades faster than true value.

- Look for a cheaper version: Can you get 80% of the value for 50% of the cost?

1. Set Clear Financial Goals

Define Your Objectives

Start with specific targets. "Build wealth" is too vague to guide daily behavior. "Invest $500 per month," "save a six-month emergency fund," or "max out my Roth IRA" gives you something concrete to protect when temptation shows up. If you want a single number that ties all of this together, read why your savings rate matters so much.

Create a Timeline

Break each goal into milestones with deadlines. A timeline turns abstract discipline into visible progress, which makes delayed gratification easier because you can see what your patience is buying.

Reward Yourself Strategically

Delayed gratification does not mean never enjoying money. It means choosing rewards that do not sabotage the main goal. A small planned treat after hitting a savings milestone is different from blowing up a month of progress with unplanned spending.

Building the Habit of Delayed Gratification

Delayed gratification is easier when you reduce decision fatigue. Automate transfers on payday, keep investing contributions scheduled, remove saved cards from your favorite shopping apps, and unsubscribe from promotional emails that trigger impulse spending. Good systems reduce the number of moments where you need raw discipline. If consistency is your weak point, use automated savings to make patience your default instead of a daily choice.

Another useful habit is to name the trade-off out loud. Instead of saying, "It is only $100," say, "This is $100 I am choosing not to invest." That framing makes the real cost harder to ignore.

Examples of Delayed Gratification in Personal Finance

- Driving your current car longer: A few more years without a car payment can free up thousands for investing.

- Skipping constant lifestyle upgrades: As income rises, investing the gap instead of spending it is one of the fastest ways to build net worth. If that pattern feels familiar, this guide to avoiding lifestyle inflation breaks down how to stop it.

- Paying off high-interest debt first: Choosing debt payoff over discretionary spending creates a guaranteed return by cutting interest costs.

- Staying invested during market declines: Patience during uncomfortable periods often matters more than finding the perfect entry point.

Overcoming the Challenges

Resisting immediate temptations is not always easy. The best response is not guilt. It is better design. Build a process that makes good decisions easier than bad ones.

- Identify triggers: Notice when you overspend most often, such as late at night, after stressful days, or when scrolling social media.

- Stay accountable: Share your goals with a partner, friend, or coach who can help you slow down big decisions.

- Visualize success: Keep your target account balance, debt-free date, or investing goal visible so the long-term reward feels real.

2. Implement Smart Investment Strategies

Diversify Your Portfolio

Spread your investments across different asset classes to manage risk and reduce the temptation to make emotional all-or-nothing bets. Diversification supports patience because it makes your plan easier to stick with during rough markets. For common behavior traps that derail long-term investors, review these common investing mistakes.

Focus on Long-Term Growth

Prioritize investments with durable long-term return potential instead of chasing whatever is surging right now. Wealth accumulation usually comes from consistency, not excitement.

Monitor and Adjust

Review your portfolio on a schedule, not based on emotion. Rebalance when needed, keep fees low, and make changes because your plan changed, not because the market made you uncomfortable.

Frequently Asked Questions About Delayed Gratification and Wealth Building

How does delayed gratification help build wealth?

Does delayed gratification mean never spending money on fun?

What is a good waiting period before buying something?

Should I invest first or pay off debt first?

Conclusion: Embrace the Power of Patience

Delayed gratification is not about deprivation. It is about buying more choice later with the discipline you use today. When you evaluate purchases through the lens of opportunity cost, automate good habits, and invest consistently, patience stops feeling passive and starts working like a wealth-building tool.

You do not need perfect self-control to benefit. You need a repeatable process that helps you make a few better decisions each week. Over time, those decisions compound into real money, more flexibility, and a much stronger financial position.